Navigating post-service benefits can be challenging, especially when it comes to life insurance. VA life insurance rates can be surprisingly affordable, but also confusing if you don’t know what you’re looking for. There are multiple programs to sort through, changing eligibility requirements, and the differences between insurance coverage provided by the Department of Veterans Affairs. Making sense of it all can feel like a puzzle.

So, whether you are considering life insurance for the first time or you are switching from Servicemembers’ Group Life Insurance (SGLI), it is important to understand how the rates work. The Department of Veterans Affairs offers specialized insurance coverage for veterans, providing unique benefits and options related to service-connected disabilities. Here is what you need to know about choosing the plan that will protect your family best.

What Is VA Life Insurance?

Understanding VA life insurance is the first part of the puzzle. These insurance programs are provided by Veterans Affairs and refer to a range of services and life insurance programs specifically designed for military service members, veterans, and eligible family members.

In the past, these included plans like Servicemembers’ Group Life Insurance (SGLI), Veterans’ Group Life Insurance (VGLI), and the S-DVI program (Service-Disabled Veterans Insurance). However, in 2023, the VA introduced the VALife program. This new program replaced the S-DVI program and offers guaranteed acceptance whole life coverage for veterans with a service-connected disability.

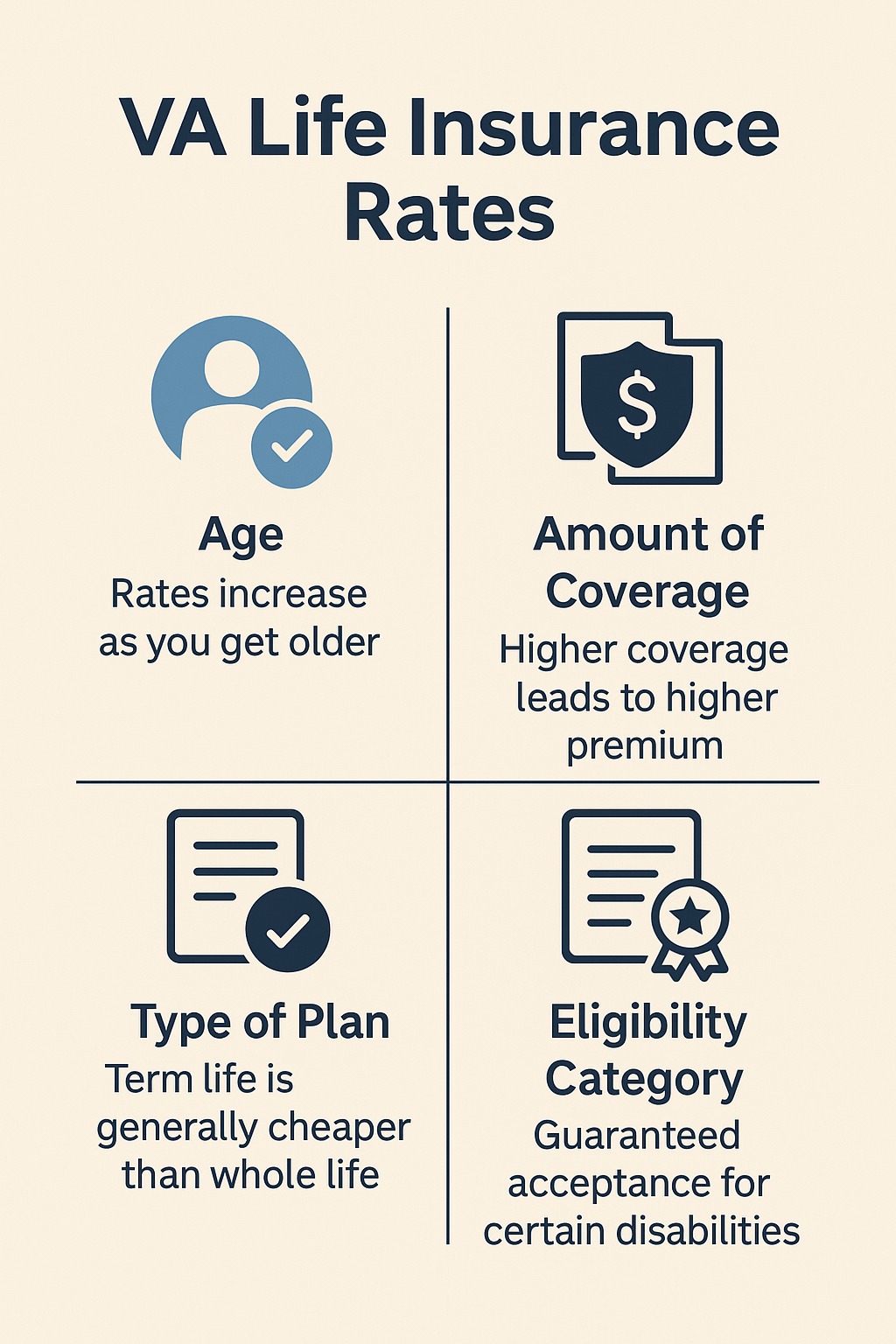

How VA Life Insurance Rates Are Determined

Several factors go into calculating the cost of VA life insurance. Typically, the VA tries to keep the rates competitive, especially for veterans with service-connected health issues. These individuals might have trouble obtaining private life insurance due to their health conditions.

That said, there are some key elements that will determine your premium. These include:

- Age: Most VA life insurance programs are age-banded, meaning rates increase as you get older. The premium rate is based on your age at the time of application and is locked in once established.

- Amount of coverage: The more coverage you want, the higher the monthly premium. The amount of coverage you select directly impacts your premium rate.

- Type of plan: Term life insurance is a form of life insurance that is usually cheaper than whole life. Some plans may offer premium waivers under certain conditions, such as total disability.

- Eligibility category: Veterans with service-connected disabilities may qualify for special programs with guaranteed acceptance and no medical exam.

For plans like VALife, age is the primary determining factor. There are no medical underwriting requirements.

Term vs. Whole Life Options for Veterans

VA term life insurance (VGLI) provides life insurance coverage for a set period and is often associated with low cost premiums initially. Veterans are able to convert SGLI coverage to VGLI within one year and 120 days of discharge.

SGLI coverage is a form of low cost term life insurance provided automatically to service members during active duty, with premiums typically deducted from a service member’s base pay. Rates for VGLI go up in five-year age bands, so the prices increase as you get older.

Whole life insurance, such as VALife and S-DVI, provides full coverage for life and builds cash value over time. The full coverage amount is paid to beneficiaries upon the insured’s death. As mentioned above, VALife is a newer option. It offers full coverage amounts up to $40,000 for service-connected disabled veterans with guaranteed approval.

For veterans with permanent disabilities, VA whole life insurance rates under VALife offer a no-hassle option, especially if private insurers have denied you. S-DVI is being phased out, as a result, but some veterans might still hold policies, and they are valid.

Current VA Life Insurance Rate Examples

If you are wondering about the current rates for VA life insurance, there is some information based on available VA tables.

For example, with VGLI term life insurance, a 45-year-old veteran might pay around $40/month for $100,000 in coverage. A 65-year-old might pay $170/month for the same amount.

VALife whole life insurance, on the other hand, might see a 60-year-old pay around $80/month for $10,000 in whole life coverage. At the same time, a 70-year-old might pay closer to $110/month for the same amount.

VALife premiums are fixed based on your age at enrollment and the coverage amount you choose, and only VALife premiums are required to maintain your coverage. The first premium payment is required to activate your coverage. VALife coverage starts after a two-year waiting period, provided premiums are paid during this time.

If the insured dies during the waiting period, the premiums paid plus interest are returned to the beneficiary. Full VALife coverage becomes effective after the two-year waiting period.

Factors That Affect VA Life Insurance Premiums

What many people focus on when it comes to life insurance is the premium. They want to know how much will come out of their pocket month-to-month. There are several factors that will impact your VA life insurance premiums.

- Your age: As stated above, premiums often go up as you get older, especially in term life programs like VGLI.

- Disability status: Veterans with any disability rating due to a service connected disability may be eligible for guaranteed whole life insurance under VALife. Applicants may need to provide proof of their disability rating as part of the application process.

- The type of policy: While term life is usually cheaper upfront, whole life will provide you with more long-term value and stability.

- Coverage amount: More coverage translates to higher monthly costs.

- Conversion deadlines: Missing your VGLI conversion window can cause you to lose eligibility and face higher rates in the private market. However, for some VA life insurance programs, there is no time limit for applying, so eligible veterans may be able to apply at any time after separation.

For veterans who missed deadlines or were denied private insurance due to medical issues, VA-backed programs can offer a second chance at affordable coverage, as long as they can provide proof of eligibility.

Comparing VA Rates to Private Insurance Plans

When it comes to affordability, VA life insurance costs are often competitive, but not always cheaper. In some cases, especially for younger and healthier veterans, private term life plans may offer lower premiums than VGLI. However, private plans require full medical underwriting, which may disqualify veterans with chronic conditions or disabilities.

Here’s how VA and private plans typically compare.

- VA Plans (VGLI/VALife): There is no medical exam required. However, there is guaranteed acceptance with some plans. Insurance coverage from Veterans Affairs includes specific services and benefits tailored for veterans and their beneficiaries, such as support programs and assistance with claims. Term plans will see rate increases with age, while whole life plans will build cash value.

- Private insurance: Medical exams are typically required, and there is no guaranteed acceptance. You will see rate increases with age with private plans, and some will build cash value, but you need to ensure you’re getting a plan that fits your needs. It’s also important to note that private plans won’t always have disability considerations either. Private insurance coverage may offer different services, but may not include the same level of support for veterans or their beneficiaries.

For many veterans, VA plans can act as a financial safety net when private insurance isn’t available or affordable. Beneficiaries are the individuals who receive the insurance payout upon the insured’s death, and both VA and private plans require you to designate a beneficiary to ensure the proper distribution of benefits.

How to Choose the Best VA Life Insurance Policy

To choose the right life insurance plan as a veteran, there are several things you should take into consideration. First and foremost, your age and health come into play. Generally speaking, if you’re under 40 and in good health, you might be able to find lower premiums than VGLI. Older individuals or those with service-connected disabilities might be better off with VALife, especially considering the VALife application process is straightforward and offers guaranteed acceptance.

When applying, review the VALife benefits, such as the two-year waiting period, guaranteed full coverage after that period, and flexible amount of coverage options.

The length of time you want coverage for also plays a factor. If you only want protection for 10 to 20 years, term life insurance is the most cost-effective option. Whole life is the better choice if you’re looking for something that lasts until death and provides full coverage for your beneficiaries.

Other important things to consider are who your dependents are and how much they’d need if you passed away. When selecting a plan, carefully consider the amount of coverage you want and whether you need full coverage from your policy. You should use the VA life insurance premium calculator to estimate your monthly premium payment and take time to pinpoint your budget, as regular premium payments are required to maintain coverage.

Also, keep in mind that some VA plans are designed to offer low cost options for veterans. And don’t forget to factor in other benefits, like pensions or VA survivor benefits, as well. This way, you can choose a plan that will suit your needs best.

FAQs About VA Life Insurance Rates

When it comes to VA life insurance rates, there are a lot of questions that come up. Here are some of the things veterans find themselves wondering about the most.

- How much is VA life insurance per month? As with any other life insurance policy, rates will vary based on several factors, like your age, type of plan, and desired coverage. The premium rate for VGLI term life policies might start around $40 per month. The VALife program, which is a whole life insurance option, has a premium rate that is based on your age at the time of application and the full coverage amount you select. For older veterans, VALife premiums could cost $80 to $150 per month, depending on age and coverage. Once set, the premium rate does not increase over time.

- Are VA life insurance rates better than private ones? A lot of the time, VA life insurance rates are better than private ones. This is especially the case for veterans with disabilities or medical issues. That said, younger, healthy veterans might be able to find cheaper options in the private sector.

- Does VA offer whole life insurance? The VALife program is a relatively new offering, as of 2023. It is a whole life insurance program with guaranteed approval for veterans with service-connected disabilities. The life insurance coverage provided by VALife includes a full coverage amount that is paid to your beneficiaries after the required waiting period or upon your death.

- Can I switch from VGLI to VALife? You cannot switch directly, but you can apply for the VALife program separately if you’re eligible. Both can be held simultaneously. Premiums must be paid regularly to maintain coverage, and there are no premium waivers available for VALife, so all premiums must continue to be paid for the policy to remain active.

- What if I missed the deadline to convert SGLI to VGLI? You may not be able to get VGLI, but you can still apply for the VALife program if you have a service-connected condition. The VA also provides a range of services to help veterans and their families understand and manage their life insurance coverage options.

Veterans Deserve Peace of Mind

Choosing the right life insurance policy for you goes beyond the numbers on the page. You want to make sure that you are protecting your legacy and providing your family with what they need in the event of your death. It can provide you and your loved ones with peace of mind. No matter what you are looking for, the options available to veterans today are designed to be more inclusive and adaptable than ever.

Take the time to check your eligibility, estimate your premiums, and weigh out your options. With detailed information, you can feel more confident with your decision. For the most part, VA-backed life insurance may not always be the lowest cost option. However, many veterans find it to be the most secure and dependable choice in the bunch.

Ready to see what works best for you? Let AllVeteran.com help you explore your options and take the next step in protecting your family’s future.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.