You need 40 Social Security credits to qualify for retirement benefits—about 10 years of work. If you’re short, you have real options, but the right one depends on your age, your work history, and whether you’re heading toward retirement or a disability claim. This guide walks through both paths, the current 2026 numbers, and what to do if the math doesn’t work out.

Key Takeaways

- One Social Security credit costs $1,890 in covered earnings in 2026, and you can earn a maximum of 4 credits per year with $7,560 in earnings (SSA).

- For retirement: you need 40 credits (roughly 10 years of work). More than 40 doesn’t increase your benefit. Your monthly payment is based on your highest 35 years of earnings, not your total credits.

- For SSDI (disability): credit requirements scale with your age. Workers under 24 may qualify with just 6 credits in the prior 3 years. Workers 31 and older need 20 credits in the past 10 years.

- If you’re short and can still work, even part-time earnings count—credits are based on annual wages, not hours.

- If you can’t work and don’t have enough credits, SSI is the federal fallback. In 2026, the maximum SSI payment is $994/month for an individual and $1,491/month for a couple (SSA).

- WEP and GPO were repealed in January 2025. Public-sector retirees with pensions from non-covered work no longer have their Social Security checks reduced.

What Social Security Credits Actually Are

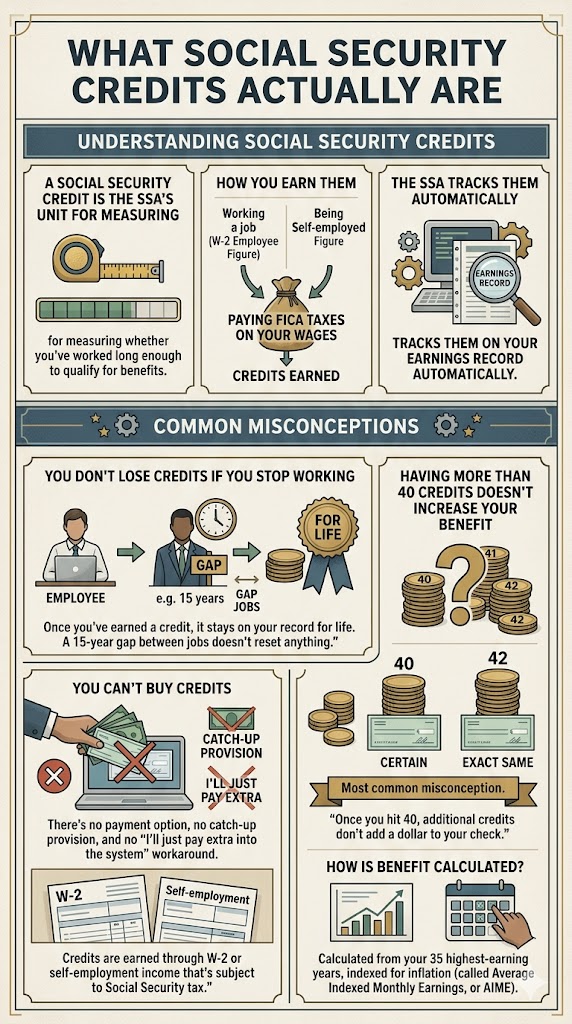

A Social Security credit is the Social Security Administration’s unit for measuring whether you’ve worked long enough to qualify for benefits. You earn them by working a job (or being self-employed) and paying FICA taxes on your wages. The SSA tracks them on your earnings record automatically.

Some Common Misconceptions:

You don’t lose credits if you stop working. Once you’ve earned a credit, it stays on your record for life. A 15-year gap between jobs doesn’t reset anything.

You can’t buy credits. There’s no payment option, no catch-up provision, and no “I’ll just pay extra into the system” workaround. Credits are earned through W-2 or self-employment income that’s subject to Social Security tax.

Having more than 40 credits doesn’t increase your benefit. This is the most common misconception. Once you hit 40, additional credits don’t add a dollar to your check. Your benefit is calculated from your 35 highest-earning years, indexed for inflation (this is called your Average Indexed Monthly Earnings, or AIME).

How Many Credits You Need

The number of credits required depends on which benefit you’re applying for.

For Retirement Benefits

40 credits, full stop. Since most people earn the maximum 4 per year, that’s typically about 10 years of work. The credits don’t need to be consecutive. Someone who worked 6 years in their twenties, took 15 years off, and worked 4 more years in their forties is at 40 credits and qualifies.

For SSDI Disability Benefits

This is where it gets confusing, because SSDI has two separate tests you have to pass.

1. The recent work test: were you working recently enough?

| Age when disability began | Recent work credits needed |

| Before age 24 | 6 credits earned in the 3 years before disability |

| Age 24 to 30 | Credit for working half the time between age 21 and your disability onset (so disability at 27 = 12 credits in the prior 6 years) |

| Age 31 and older | 20 credits in the 10 years immediately before disability |

2. The duration of work test: have you worked long enough overall? This is a sliding scale based on age, ranging from 6 credits for workers in their early twenties to 40 credits for workers 62 and older. The SSA’s duration table shows the exact requirement by age.

You have to pass both tests to qualify for SSDI. This is why two workers with the same total credits can get different answers: the timing of those credits matters as much as the count.

What Counts as Work That Earns Credits

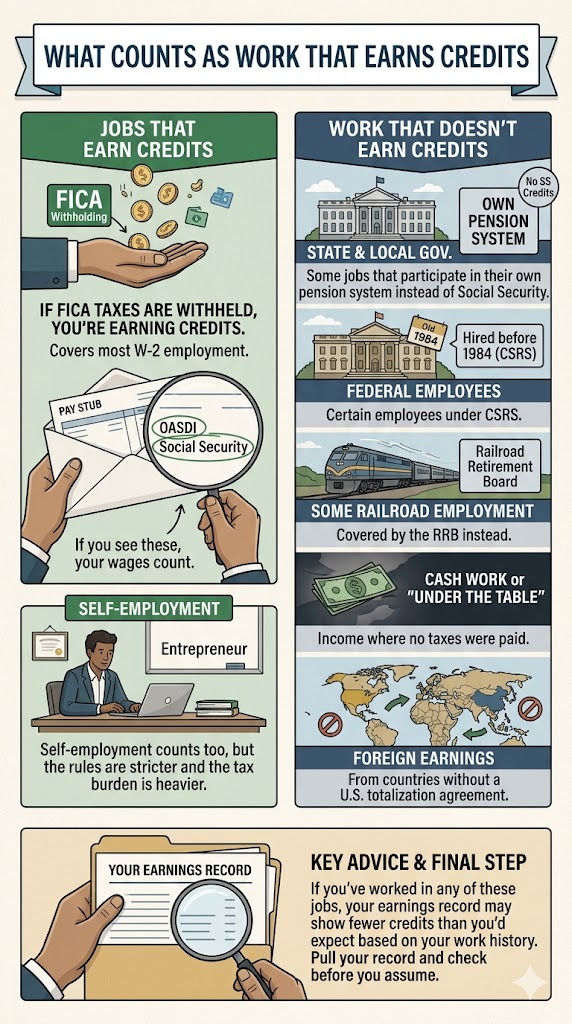

If your job withholds FICA taxes from your paycheck, you’re earning credits. That covers most W-2 employment. If you see “OASDI” or “Social Security” as a line item on your pay stub, your wages count.

Self-employment counts too, but the rules are stricter and the tax burden is heavier — see the next section.

A few categories of work don’t earn Social Security credits:

- Some state and local government jobs that participate in their own pension system instead of Social Security

- Certain federal employees hired before 1984 (CSRS)

- Some railroad employment (covered by the Railroad Retirement Board instead)

- Cash work or “under the table” income where no taxes were paid

- Foreign earnings from countries without a U.S. totalization agreement

If you’ve worked in any of these jobs, your earnings record may show fewer credits than you’d expect based on your work history. Pull your record and check before you assume.

Important update for public-sector workers: WEP and GPO are gone

Before January 2025, two provisions—the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO)—reduced Social Security benefits for people who also received a pension from non-covered work. Teachers, firefighters, police officers, and certain federal employees were the most affected.

The Social Security Fairness Act, signed January 5, 2025, repealed both. The last month WEP and GPO applied was December 2023, so anyone affected should already be receiving full benefits or back pay. As of mid-2025, the SSA had issued over $17 billion in retroactive payments to 3.1 million people.

If you’ve been planning your retirement around a reduced Social Security benefit because of WEP or GPO, that calculation no longer applies. Check your most recent benefit statement.

Credits if You’re Self-Employed

The math is the same ($1,890 per credit in 2026, max 4 per year) but the tax mechanics are different.

When you work a W-2 job, your employer withholds 6.2% for Social Security and matches it with another 6.2%. As a self-employed worker, you pay both sides: the full 12.4% as self-employment tax. That’s what funds your credits.

This is where a lot of self-employed workers undercut their own future benefits. Heavy itemized deductions reduce your taxable self-employment income, which reduces the earnings reported to Social Security, which reduces both your credits and your eventual benefit amount. The short-term tax savings come at a long-term cost.

If you’re self-employed and want to make sure you’re earning all 4 credits each year, you need to report at least $7,560 in net self-employment earnings (gross income minus business expenses) for 2026. That’s the floor for maximum credits.

What To Do If You’re Short on Credits

This is the part most generic guides skip. Here’s how to think about it based on what’s actually going on in your situation.

Scenario 1: You’re near retirement and a few credits short

If you’re 60+ and only 4 to 12 credits short of 40, the cleanest fix is usually to keep working. Even part-time work that pays $7,560 in 2026 gets you the full 4 credits. Two more years of part-time work can close the gap.

A common mistake: filing for early retirement at 62 thinking you’ll “lock in” benefits. If you don’t have 40 credits yet, you can’t draw retirement benefits at all — and filing early permanently reduces what you’ll receive once you do qualify. If you’re short, work the extra time. The math almost always favors waiting.

Scenario 2: You worked, but mostly under the table

This is one of the toughest situations. Cash wages that weren’t reported to the IRS don’t appear on your earnings record, and there’s no retroactive fix. The only path forward is to start reporting current and future income (either as W-2 wages or as self-employment income). Credits earned at 55 still count.

If you’re past working age and have no path to 40 credits, your fallback is SSI. See Scenario 4.

Scenario 3: You’re a divorced or widowed spouse with limited work history

You may not need credits of your own. If you were married for at least 10 years and your ex-spouse qualifies for Social Security, you can claim a divorced-spouse benefit based on their record — even if they’ve remarried. Widows and widowers can claim survivor benefits as early as age 60. Your own credits don’t have to clear the 40-credit bar for these benefits.

This is one of the most underused paths in the Social Security system. If your work history is sparse but you were married for a decade or more, check this before assuming you have no options.

Scenario 4: You’re disabled (or older) and can’t work to make up credits

If you’re 65+, blind, or disabled, and you don’t have enough credits for SSDI or retirement, Supplemental Security Income (SSI) is the federal program that fills the gap. SSI is need-based and therefore doesn’t require any work credits at all, but it has strict income and asset limits.

In 2026, the maximum federal SSI payment is $994/month for an individual and $1,491/month for a couple (SSA). To qualify, your countable resources must be under $2,000 (individual) or $3,000 (couple). These limits have been unchanged since 1989. Most states add a small supplemental payment on top.

SSI and SSDI aren’t mutually exclusive. Some people qualify for both (called “concurrent benefits”) when their SSDI payment is below the SSI threshold.

What Your Benefit Will Actually Be

Here’s where the original misconception about credits matters most: the number of credits you have doesn’t determine your benefit amount. It only determines whether you qualify.

Your benefit is calculated from your 35 highest-earning years (indexed for inflation). If you worked 38 years, the SSA uses the best 35 and drops the rest. If you worked only 28 years, the formula uses zeros for the missing 7 years, which drags your average down significantly.

A Few 2026 Reference Numbers:

- The average retired worker receives about $2,000/month in 2026, reflecting the 2.8% COLA.

- The average SSDI recipient receives about $1,630/month.

- The maximum Social Security retirement benefit at full retirement age (FRA) is $4,018/month in 2026 — but reaching it requires earning at or above the Social Security wage base for 35 years.

- The maximum SSDI benefit is $4,152/month, though most recipients receive far less.

Full Retirement Age (FRA): What Changed

For anyone born in 1960 or later, FRA is 67. That phase-in completed in 2026 — the last year FRA was anything other than 67 was for people born in 1959 (FRA of 66 years, 10 months).

Filing Earlier Permanently Cuts Your Benefit:

- File at 62 (the earliest age): your benefit drops to 70% of your full amount

- File at FRA (67): you get 100%

- Delay past FRA: you earn delayed retirement credits worth 8% per year, maxing out at age 70 with a benefit equal to 124% of your FRA amount

The choice between filing at 62, 67, or 70 is one of the biggest financial decisions most people will make. If you’re healthy and don’t need the income immediately, waiting almost always pays.

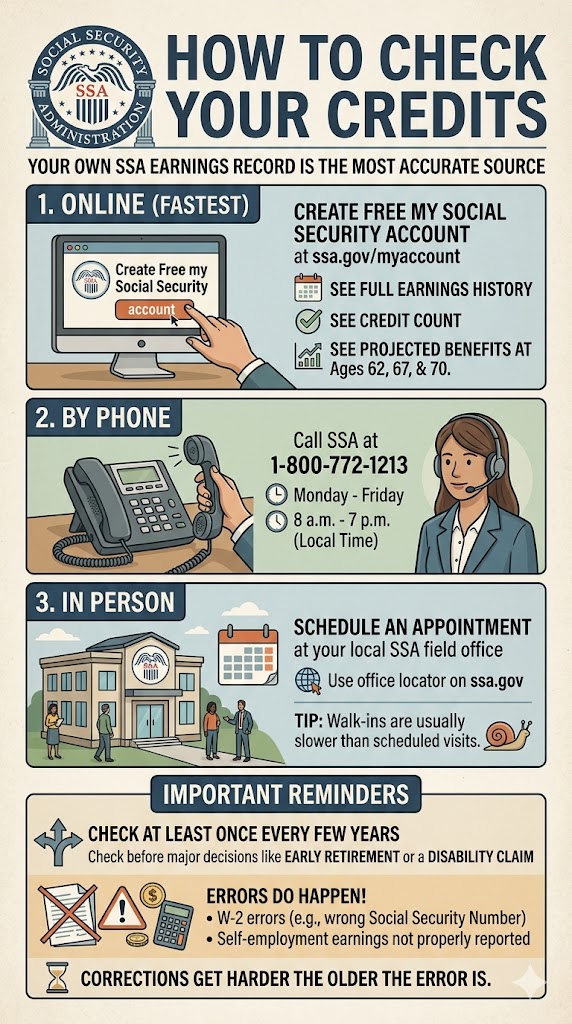

How to Check Your Credits

The most accurate source is your own SSA earnings record. There are three ways to get it:

- Online (fastest): Create a free my Social Security account at ssa.gov/myaccount. You’ll see your full earnings history, credit count, and projected benefits at 62, 67, and 70.

- By phone: Call SSA at 1-800-772-1213, Monday through Friday, 8 a.m. to 7 p.m. local time.

- In person: Schedule an appointment at your local SSA field office (use the office locator on ssa.gov). Walk-ins are usually slower than scheduled visits.

Check your record at least once every few years — and especially before any major life decision like early retirement or a disability claim. Errors do happen, particularly with W-2s that listed the wrong Social Security number or self-employment earnings that weren’t properly reported. Corrections get harder the older the error is.

Frequently Asked Questions

How Many Social Security Credits Do I Need to Retire?

You need 40 credits to qualify for Social Security retirement benefits, which typically takes about 10 years of work. Having more than 40 credits doesn’t increase your benefit amount; that’s calculated from your highest 35 years of earnings, not your total credits.

Can I Buy Social Security Credits?

No. Social Security credits cannot be purchased, transferred, or paid for directly. They can only be earned through wages or self-employment income that’s subject to Social Security tax.

How Much Do I Need to Earn for One Social Security Credit in 2026?

In 2026, you earn one Social Security credit for every $1,890 in covered earnings, up to a maximum of 4 credits per year. To get the full 4 credits, you need at least $7,560 in earnings for the year.

What Happens if I Don’t Have Enough Credits for Social Security?

If you can still work, even part-time wages count toward credits. If you can’t work and you’re 65+, blind, or disabled, you may qualify for Supplemental Security Income (SSI), which has no credit requirement. Divorced or widowed spouses may also qualify for spousal benefits based on a former or deceased spouse’s record without needing 40 credits of their own.

Do Social Security Credits Expire?

No. Once you’ve earned a credit, it stays on your record permanently. Long gaps in employment do not erase credits you’ve already earned. The only exception is for SSDI’s “recent work test,” which requires that some of your credits were earned in a specific window before your disability began.

What’s the Difference Between SSDI and SSI?

SSDI (Social Security Disability Insurance) is based on your work credits and earnings record. SSI (Supplemental Security Income) is a need-based program for low-income people who are 65+, blind, or disabled. SSDI requires credits; SSI doesn’t. The two can be received concurrently if your SSDI payment is low enough.

Does the Windfall Elimination Provision Still Reduce my Benefit?

No. WEP and GPO were repealed by the Social Security Fairness Act, signed into law on January 5, 2025. The last month they applied was December 2023. If you have a pension from non-covered work, your Social Security benefit is no longer reduced because of it.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.