Supplemental Security Income (SSI) is a federal needs-based program designed to provide financial assistance to low income people who are aged, blind, or disabled and who have limited income and resources. An SSI recipient is someone who meets the program’s strict financial criteria, including income and asset limits, and is eligible to receive benefits.

Unlike Social Security Disability Insurance (SSDI), which is based on work history and contributions to Social Security, SSI eligibility depends heavily on financial need. One of the most important components of this eligibility test is the asset limit.

The SSI Asset Limit

The SSA sets strict SSI asset limits on the amount of countable resources an individual or couple may have and still qualify for SSI. These asset limits determine how many assets you can own and remain eligible for benefits.

• Individual limit: $2,000 — A single person can have up to $2,000 in countable assets and still qualify for SSI.

• Couple limit (married and living together): $3,000 for a couple — A married couple can have up to $3,000 in combined countable assets.

These SSI asset limits have remained unchanged for decades, despite increases in living costs. The rule reflects SSI’s design as a need-based safety net program—its goal is to help only those with very limited means.

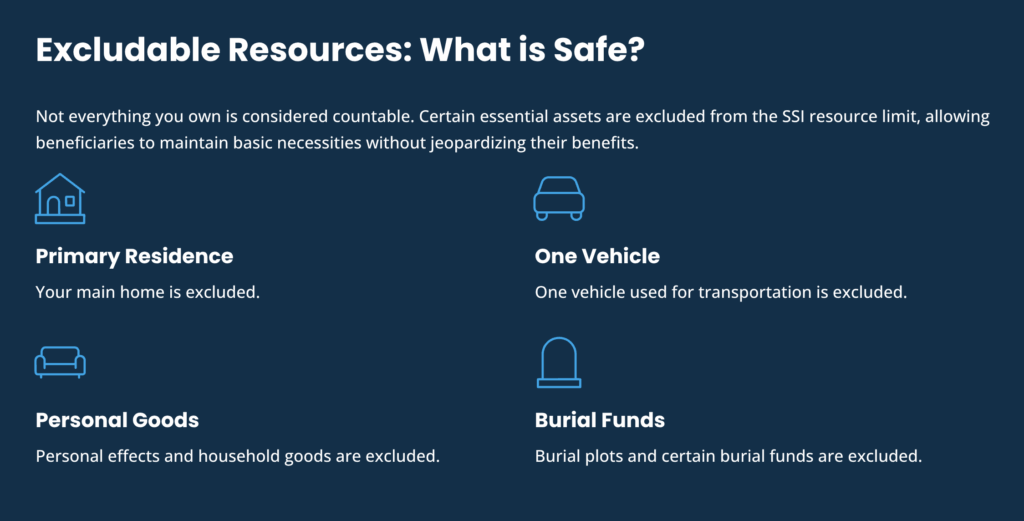

Which Assets Count?

A resource is anything you own that could be converted to cash and used for food or shelter. These resources are also referred to as assets. However, not everything you own is considered countable. The SSA divides resources into countable and excludable categories.

Countable Resources Include:

• Cash on hand (money you keep at home or in your wallet).

• Bank accounts (checking, savings, certificates of deposit, etc.). A bank account is a type of resource that counts toward the SSI resource limit.

• Stocks, bonds, and mutual funds.

• Non-home real estate (land or property other than your primary residence).

• Retirement accounts (IRAs, 401(k)s, pensions) if they can be accessed.

• Vehicles beyond the first (with some exceptions).

• Life insurance policies with a cash surrender value greater than $1,500.

These assets count toward the SSI resource limit, and exceeding the limit may affect your eligibility.

Excludable Resources Include:

• Primary residence.

• One vehicle used for transportation.

• Personal effects and household goods.

• Personal property that is not counted as a resource.

• Burial plots and certain burial funds.

• Some life insurance policies if the total face value is $1,500 or less.

Savings and the Asset Limit

Savings are one of the most common reasons applicants exceed the SSI resource limit. When determining eligibility for SSI, both income and resources are considered, and exceeding the allowed thresholds can result in disqualification.

Examples:

• If an individual has $1,900 in a savings account and keeps $200 in cash, these resources exceed the $2,000 limit and would not qualify.

• Even modest assets in accounts may push you over the threshold.

Some individuals use special needs trusts or ABLE accounts (Achieving a Better Life Experience accounts) to set aside funds without jeopardizing SSI eligibility, as these options are designed to help manage asset limits.

4. Property Ownership and SSI Benefits

Property can have a major effect on eligibility.

• Your primary residence is excluded.

• Other real estate counts unless excluded.

• Only one vehicle is excluded. Extra cars may count.

• Certain personal property, such as household goods, and burial spaces for yourself or immediate family, are excluded.

When determining eligibility, assets count toward the SSI resource limit unless specifically excluded.

Example: If you own your home, one car, and also have a small parcel of land worth $4,000, you would be over the limit and ineligible unless you sell or dispose of the land.

Income and Its Impact on Resources

Income and resources are separate tests, but they interact. Income is what you receive monthly, and if unspent, it becomes a resource the following month. Your monthly income and income limits directly affect your eligibility for SSI, as you must have income below a certain threshold to qualify.

Types of Income:

• Earned income (wages, self-employment, or income from a part time job). Earned income is counted toward your SSI income and is subject to income limits for eligibility.

• Unearned income (pensions, Social Security benefits, unemployment benefits, gifts). Both earned and unearned income are considered when calculating your countable income, which must not exceed the countable income limit set by SSI rules.

• In-kind support (free food or shelter). If someone helps pay your rent or utilities, this can reduce your SSI benefits due to in-kind support and maintenance rules.

Exclusions:

• The first $20 of most unearned income is excluded, and the first $65 of earned income plus half the remainder is excluded. This means a certain amount of your income does not count toward the income limit.

• Some assistance (SNAP, housing subsidies, small irregular gifts) may not affect eligibility.

Countable income is the portion of your income that the Social Security Administration uses to determine eligibility and benefit amounts. The countable income limit is the maximum amount of countable income you can have and still receive SSI benefits. Your living arrangement, such as whether you live alone or with others, also impacts your benefit calculations and SSI benefits amount.

If you are married, your spouse’s income is considered in the eligibility process, and a spouse who does not qualify for SSI can still affect your benefit amounts through spousal deeming. The maximum amount of income you can have and still receive SSI is based on federal and state income limits, which may be increased by a state supplement or supplemental payments in some states.

SSI benefits are paid monthly, and the SSI check you receive is based on your countable income, living arrangement, and other factors. Benefit amounts may be increased by state supplement programs or other supplemental payments. To receive SSI or continue receiving SSI, you must meet all income and resource requirements, have a qualifying disability. More than half of SSI recipients have no income, which highlights the strict income limits for eligibility.

Other programs, such as Medicaid and state supplements, interact with SSI and can affect your eligibility or benefit amounts. If you receive other benefits, your SSI benefits amount may change if your income or living arrangement changes.

Planning Around the SSI Asset Limit

Because the SSI resource limit is so restrictive, many beneficiaries, especially people with disabilities, use strategies to remain eligible:

• Special Needs Trusts (SNTs). Certain expenses, such as travel, recreation, and medical bills, can be paid directly by the trust without affecting eligibility.

• ABLE Accounts.

• Spend-down strategies (medical expenses, home repairs, debt repayment).

Why the Rules Matter

Failing to comply can result in:

• Denial of the application.

• Overpayment demands.

• Suspension of benefits until resources are reduced.

SSI provides a lifeline to individuals with disabilities and limited means. However, eligibility is tightly controlled by the asset limit of $2,000 for individuals and $3,000 for couples.

By learning the rules, using available exclusions, and exploring planning tools, applicants can preserve financial security without jeopardizing SSI eligibility.

At Benefits.com, we are here to help you navigate the process and receive the benefits you deserve. Begin today by taking our free eligibility quiz.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.