As a parent with a disabled child, you want to know that your child will be cared for when you can no longer provide or manage the care yourself. There are many financial tools that help families with special needs planning for the life of their child. A Special Needs Trust is one method that can ensure your child has the funds needed to live a full life after you are gone.

Mechanics of the Special Needs Trust

There are several forms that a Special Needs Trust can take. First of all, the trust can cover assets directly owned by the disabled individual, which is a called a first person trust. These trusts often include funds from legal settlements, or other direct income for the individual. The second primary type is a third party trust where the assets are technically owned by another person, but held in trust to be spent and managed for the benefit of the disabled person.

A key distinction is that if assets are directly owned by the disabled person, in a first person trust, that money can count as “resources” to be spent down before the person is eligible for Medicaid or other government benefits. However, parents or guardians can set up a third party trust where they transfer assets to be held in trust for the benefit of the disabled child, without counting as “resources.”

It is fully legal, and encouraged, for parents to plan for their disabled children’s needs this way. Government assistance is often enough to pay for basic care, but funds in a third party trust can be used to supplement that care. Technically the assets are transferred to and owned by the person appointed as Trustee – who is bound to use the funds for the benefit of the disabled person – the named beneficiary.

What assets can parents put into the Special Needs Trust?

Trusts can be designed with some flexibility, to serve the financial needs of your family and the care needs of your child. In some cases, you can set up the trust on your own, with some guidance from trusted agencies or resources. In other cases, paying for the advice of a lawyer with expertise in the area may be worth it in the long run.

Trusts can be designed with some flexibility, to serve the financial needs of your family and the care needs of your child. In some cases, you can set up the trust on your own, with some guidance from trusted agencies or resources. In other cases, paying for the advice of a lawyer with expertise in the area may be worth it in the long run.

If you expect that you are likely to spend most of your retirement earnings and savings before your death, then you can set up a simple trust that would, after your death, transfer any property you own, life insurance proceeds, and any remaining funds, into the Special Needs Trust. You designate a person to act as Trustee, who has the power to sell the property and otherwise manage the assets for the benefit of your child’s care.

If you have a more complicated financial situation, or substantial forms of assets, an experienced lawyer can help advise you on the best way to structure the trust.

One common form is for parents or guardians to set up the trust as part of your estate planning package. You can establish the trust while you’re still living, and begin transferring assets into it while you’re alive; or, you can make it a part of your will, so that the trust would be established upon your death.

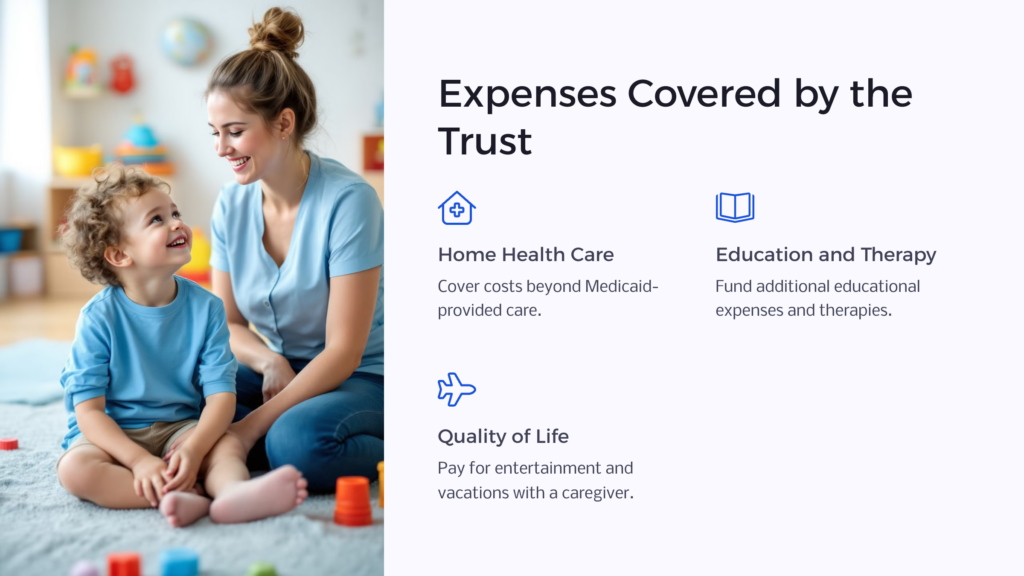

What Expenses Can the Special Needs Trust Cover?

The Social Security Administration has set out some guidelines to help when planning for spending from third party trusts. A key point – if you don’t want to lose Medicaid eligibility – is that the money can’t be given directly to the disabled person, but can be spent for their benefit. Some expenses commonly allowed from a third party trust are: costs for home health care over the care provided by Medicaid, additional therapy, or educational expenses. The money can be used for some entertainment purposes and even vacations for the disabled person and a caregiver.

Ultimately the Social Security Administration will decide what payments from a trust will be counted as income. Be sure to appoint a trustee who can monitor allowable expenses. This can be someone you know and trust, or a professional trustee.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.