| Quick Answer: Long-term disability insurance can last two, five, or 10 years, until retirement, or even for life, depending on the terms outlined in your policy. |

Understanding insurance can be tricky, especially when preparing for unexpected things like long-term disability. Long-term disability (LTD) is a type of insurance for people who can’t work for a long time due to serious health issues or injuries.

But exactly how long does long-term disability last? In this post, we’ll get answers to important questions about how long this type of insurance lasts, what long-term disability is, and how it works, plus helpful tips on how to choose the right LTD insurance for you.

What Is Long-Term Disability?

Long-term disability is a type of insurance that supports people financially when they can’t work for an extended period of time due to a serious health issue or injury. The insurance protects a percentage of your pre-disability earnings, which can help cover living costs if you cannot work.

You may be able to obtain long-term disability insurance through employment benefits or by purchasing it as a private policy. The coverage is intended to last over an extended period—until you can resume work, reach a specific age, or for a set duration outlined in the policy. Depending on the policy, this period could be two, five, or ten years, until age 65, or even for life.

Long-Term vs. Short-Term Disability

To better understand disability insurance, it’s important to know the difference between long-term and short-term disability, as they serve specific purposes in providing financial support when health issues impact your ability to work.

Long-term disability offers extended financial support for people unable to work due to serious health conditions or injuries. It offers a percentage of your pre-disability income after a waiting period, providing financial support for an extended time.

Short-term disability (STD) provides temporary financial assistance for shorter periods, typically around three to six months, covering a portion of income during temporary disability. STD bridges the financial gap during short-term health challenges before potential long-term disability benefits take effect.

How Does Long-Term Disability Work?

Now that you know long-term disability, let’s walk through how the LTD process works.

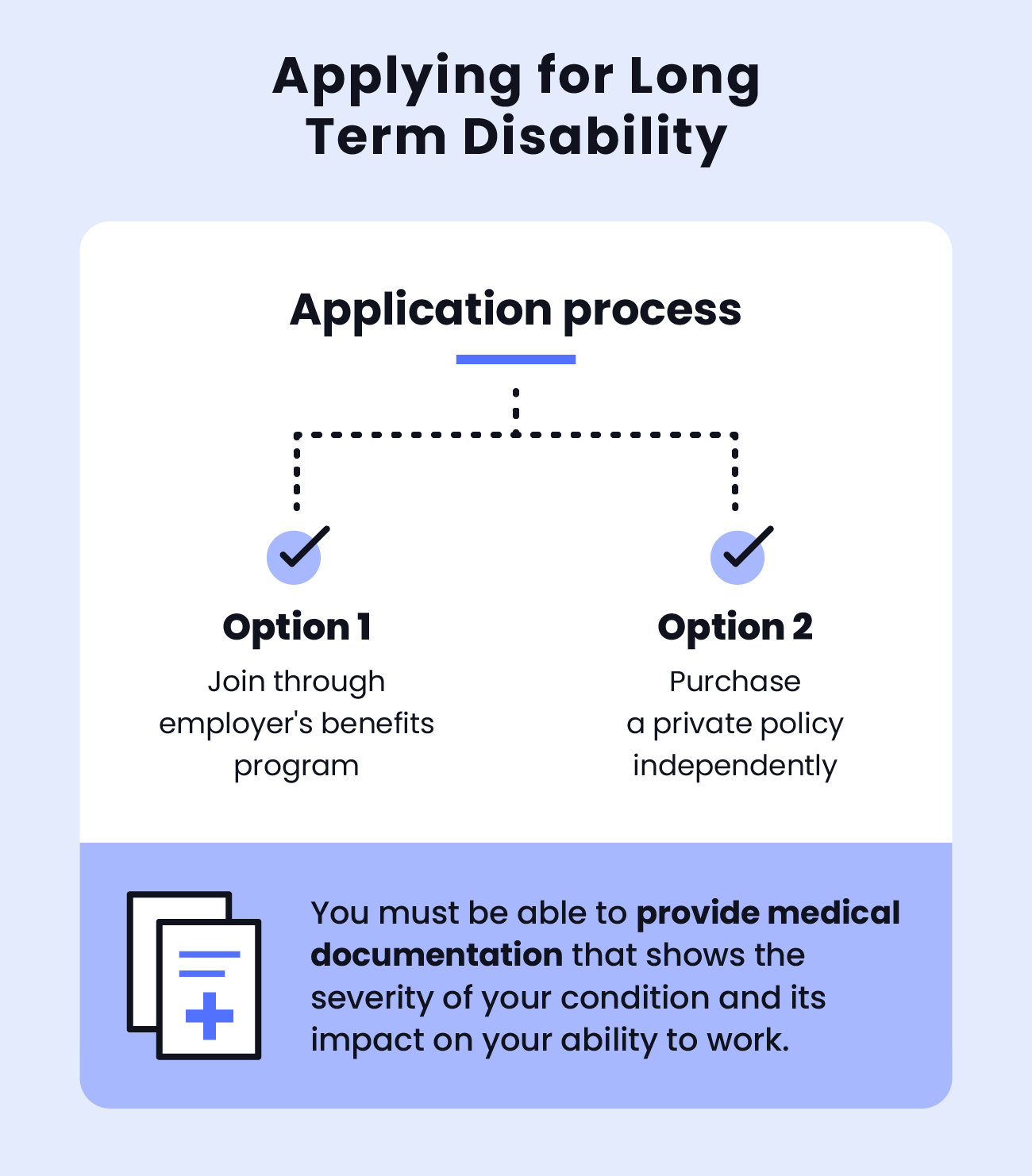

Application Process

When you apply for LTD benefits, you have two primary options: join through your employer’s benefits program or purchase a private policy. Applying through an employer often involves navigating the company’s established procedures, while purchasing a private policy can be done independently through insurance providers.

When you apply for LTD, you must be able to provide medical documentation that shows the severity of your condition and its impact on your ability to work. This documentation is a key factor in the approval process, helping insurance companies assess your eligibility for long-term disability benefits.

Approval Criteria

To qualify for LTD, you must meet specific criteria outlined by your insurance provider. Some policies may require you to meet a certain definition of disability, including:

- Own-occupation disability: You’re considered disabled if you cannot perform the specific duties of your own occupation, even if you can work in a different capacity or field.

- Any-occupation disability: You’re considered disabled only if you cannot perform any job you’re qualified for through education, training, or experience.

For instance, imagine a concert pianist who sustains a severe hand injury, limiting their ability to perform. The pianist qualifies for benefits with an insurance policy featuring an own-occupation disability definition, as they can no longer fulfill the requirements to play the piano.

Conversely, if the policy used an any-occupation definition, the pianist may not qualify, as they could potentially work in a different field.

Elimination Period

The elimination period, also known as the waiting period, is the time you must wait after becoming disabled before you’re eligible to receive benefits. If you’re still disabled according to the policy’s definition of disability at the end of the elimination period, you can start receiving benefits.

Most policies have a 90-day elimination period, but the exact duration depends on the specifics of the insurance policy. Some could be as short as 30 days, while others could last a full year.

During this period, people usually depend on short-term disability or sick leave to get financial help. The length of the elimination period is a major factor to consider when selecting a disability insurance policy.

Shorter elimination periods may result in higher premiums but quicker access to benefits, while longer elimination periods may offer lower premiums but a delayed initiation of financial support.

Benefit Calculation

LTD benefits are typically calculated as a percentage of your pre-disability income. While varying between insurance policies, this percentage generally falls between 50% and 70%.

For instance, if your pre-disability income was $4,000 monthly and the LTD policy provides 60% coverage, the monthly benefit would amount to $2,400. This calculated percentage is a key factor in determining the level of financial assistance you’ll receive while you cannot work.

It’s important to carefully review the benefit calculation details in your specific policy, as variations exist among insurance providers.

Ongoing Updates

Getting LTD benefits is an ongoing process that may require you to regularly share health updates with your employer or insurance company. These updates are important to keep getting benefits, ensuring the insurance provider knows about your health and if you can return to work.

5 Tips for Choosing the Right Long-Term Disability Insurance

Long-term disability insurance is not one-size-fits-all. Check out these top tips to help you choose the best LTD insurance:.

1. Assess Your Needs

To pick the right LTD insurance, evaluate your finances by assessing your monthly expenses, debts, and savings.

Think about how much income you’d need if you couldn’t work due to a disability. Determine the percentage of your income the policy will replace (usually between 50% and 70%).

2. Understand Your Employer’s Coverage

Check if your job includes long-term disability coverage. Know what your employer’s plan covers, the limits, and how long the benefits last. Understanding these details helps you decide if you need extra coverage and ensures you know the support available if you face a disability.

If your employer’s coverage doesn’t align with your financial needs, you can always supplement your coverage with a private policy. Coverage offered through an employer is often more cost-effective than purchasing a private policy, but you can acquire both if needed.

3. Evaluate Elimination Periods

When considering LTD insurance, it’s important to evaluate the elimination period before benefits kick in.

Shorter waiting periods mean you can access benefits sooner, but they usually come with higher premiums. This may be a better option if you don’t have short-term disability coverage, savings, or other resources to cover your expenses while waiting for LTD to kick in.

Longer waiting periods may result in lower premiums but mean a longer time without benefits. This choice could be preferable if you have short-term disability coverage, a working spouse, or sufficient savings to support you during the waiting period. In such cases, selecting an LTD plan with a longer elimination period can help lower premiums or make a longer benefit period financially manageable.

Ensure the waiting period you choose aligns with your financial situation and preferences.

4. Be Aware of How the Policy Defines Disability

When choosing LTD insurance, check how the policy defines disability. Some use “own-occupation,” considering you disabled if you can’t do your specific job, offering broad coverage. Others use “any-occupation,” where you’re considered disabled if you can’t do any job you’re qualified for, making it harder to qualify for disability benefits.

Choosing a policy based on your own occupation ensures comprehensive protection that matches your work, increasing the chances of getting benefits when needed.

5. Check the Renewability

Understanding the renewability provision in your LTD insurance policy is crucial, as it outlines when and under what conditions the insurance company can modify, cancel, or increase premiums.

Here are the four different renewability provisions commonly found in disability income insurance policies:

- Noncancelable and guaranteed renewable: This is the most favorable provision. It means the insurance company cannot cancel the policy, change the terms, or increase premiums as long as the policyholder continues to pay premiums. This offers the highest level of security and consistency.

- Guaranteed renewable: The insurance company guarantees to renew the policy as long as the policyholder pays premiums. However, the company can increase premiums for an entire group of policyholders, not just individuals.

- Conditionally renewable: The insurance company commits to renew the policy under certain conditions. These conditions could include changes in health, occupation, or other specified factors. This provision provides less certainty for policyholders.

- Optionally renewable: This provision allows the insurance company to decide whether or not to renew the policy at the end of each policy period. It provides the least assurance for policyholders.

Frequently Asked Questions

Still have questions about long-term disability insurance? Keep reading to find the answers to common questions about LTD.

1. How Much Does Long-Term Disability Pay?

The amount LTD pays varies, typically calculated as a percentage of pre-disability income, often ranging from 50% to 70%. For instance, if your pre-disability income was $10,000 monthly and the policy provides 70% coverage, the monthly benefit would be $7,000.

2. Is Long-Term Disability Taxable?

Whether LTD benefits are taxable depends on how you pay the insurance policy premiums. If the premiums were paid with after-tax dollars (meaning you paid for the coverage with your own money already taxed), then the LTD benefits are generally not taxable. In this case, the benefits provide tax-free income.

On the other hand, if the premiums were paid with pre-tax dollars (meaning you paid for the coverage with money that hasn’t been taxed yet, like through a workplace benefit plan), then the LTD benefits are usually considered taxable income. In such cases, you may need to report and pay taxes on the received benefits.

3. What Qualifies for Long-Term Disability?

What qualifies you for long-term disability depends on how your policy defines disability. If your provider defines disability as own-occupation, you can qualify for benefits if your disability prohibits you from performing your specific job.

However, if your coverage defines disability as any-occupation, then you can only qualify for benefits if your disability prohibits you from performing any job you’re qualified for.

4. What Does Long-Term Disability Cover?

Long-term disability covers a percentage of your monthly income if a disabling condition, such as an illness or injury, prevents you from working. The specific percentage is defined by your insurance provider but is generally around 50% to 70% of your monthly income.

5. How Long Does Long-Term Disability Last Through an Employer?

The duration of LTD through an employer varies based on the specific policy. It can last for a set number of years, until age 65, or for a lifetime, depending on the terms outlined in the policy.

Employees should review their employer-sponsored LTD policy details provided in their benefits package to understand how long the long-term benefits last. For precise information, contact your employer’s benefits administrator or human resources department.

Benefits.com Can Help You Find the Right Long-Term Disability Insurance

Understanding how long long-term disability lasts is crucial for making informed decisions about your financial security in the face of unexpected challenges. Whether it lasts for two years, five years, until retirement, or a lifetime, the terms outlined in your policy play a pivotal role.

At Benefits.com, our commitment is to empower every U.S. resident in navigating the complexities of disability programs, ensuring you find the optimal benefit plan tailored to your needs. Explore your eligibility through our Benefits Quiz to unlock the full potential of the benefits available.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.