Find out how to get SSI while working by using SSI work incentives and learn which work earnings reduce SSI payments and which do not.

How to get SSI while working

Earned Income and SSI

Many people want to know how to get SSI and work too. Sometimes you can do just that. Whether you continue to be eligible for SSI while working depends on two things: First, after all exclusions have been applied, your combined unearned income and countable earned income must fall below the SSI income limit, which in 2020 is less than $783.00 for individuals and less than $1,175.00 for eligible couples. Second, your work must not be substantial gainful activity.

Earned income is also factored into the determination of SSI financial eligibility as discussed below. In eligibility and benefit calculations, the first $65 of work earnings and half the excess earnings above $65 are excluded and not counted. These exclusions are in addition to a $20 general exclusion applied to work earnings if it has not been used to exclude unearned income. For example, if an SSI eligible person had only earned income of $200, his or her benefit would be calculated as follows:

Countable Income Calculation

$200.00 earned income

– 20.00 general exclusion

$180.00

– 65.00 work exclusion

$115.00

/ 2 second work exclusion

$ 57.50 countable income

Payment Calculation

$783.00 unreduced maximum federal SSI payment

– 57.50countable income

$ 725.50 SSI payable

SSI’s Definition of Earned Income

Generally speaking earned income consists of wages from a job, whether paid in cash or in another form, payments for services performed in a sheltered workshop or work activities center, net earnings from a business if a person is self-employed. It also includes royalties earned in connection with a publication, honoraria received for services rendered, and artwork if you are a self-employed artist.

SSI Work Incentives

SSI law includes several work incentives, some of which apply only to SSI recipients and not to Social Security beneficiaries. Some incentives help you to work and continue to receive SSI. Others are designed to help you eventually return to work at a level you no longer need SSI. Some of the incentives may serve both functions at one time or another. SSI work incentives include Impairment-Related Work Expenses (IRWE’s) for the disabled, work expenses for the blind, the Student Earned Income Exclusion (SEIE), the Ticket to Work, and the Plan to Achieve Self-support (PASS).

Ticket to Work

The Ticket to Work program is free and voluntary. The program connects you with a network of vocational specialists in state agencies and private companies. Some examples of services that are available through the Ticket to Work program are return-to-work planning, job-search assistance, education and training and support services that you may need to obtain and keep a job. If you are using a Ticket to Work, in some circumstances your claim will not be reviewed for medical recovery.

Plan to Achieve Self–Support (PASS)

A PASS is a written plan of action—a simple business plan—for getting a particular kind of job or for starting a particular kind of business. Like the Ticket program, a PASS can help you get a job while receiving SSI payments, or a PASS can help you start your own small business, which may be even better, since you can start a home-based business that may require no commuting, walking, communicating or other activity that may be difficult for you.

You may have a PASS approved if: 1) You are not now financially eligible for SSI but would be eligible for SSI based on disability if not for your above-the-limit income and/or assets that you want to use for a return-to-work plan; or 2) you are already eligible for SSI and have income that reduces the amount of SSI you receive

In the PASS, which must follow the format and guidelines set out by SSA and be approved by SSA. In the PASS, you state the following:

- The kind of job or business you want to work toward, that is, you state your work goal.

- The steps you will take and the things you will need in order to achieve this work goal (e.g., special education or training, equipment, supplies, workplace, child care, a vehicle, etc.) and the estimated cost of those services and goods.

- The income or assets you have that you will set aside to pay for items and services needed to reach your goal through the PASS. These might be Social Security benefits, income from a current job, child support, or savings.

- A timetable for achieving your goal.

You can get help writing the PASS from a Social Security claims representative or a vocational counselor.

If the SSA approves your plan, they will not count the money you spend on it (within limits) when determining your eligibility for SSI. Non-SSI income you spend to fund the PASS will not be countable income when calculating your SSI benefit. This will result in new SSI eligibility or in an increase your SSI benefit if you are already entitled to SSI so that the money you spend on your PASS goals will be replaced with SSI benefits to cover your shelter, food, and other basic living expenses.

Over time, using PASS to reach your work goal will help you reduce or eliminate benefits you receive from SSI, Social Security or both as you become self-supporting.

Continuation of Medicaid

In some circumstances, your Medicaid health insurance will continue if SSI ends because of your work. For Medicaid to continue, your income must be below your state’s Medicaid income limit. Your local Social Security office can tell you your state’s Medicaid income limit. There are three additional requirements: You need health insurance to continue working, that is, you cannot maintain health good enough to work without the medical services and goods that Medicaid provides. You cannot afford similar medical insurance. You continue to have a disabling condition; and you meet all SSI eligibility requirements, except for your earned income.

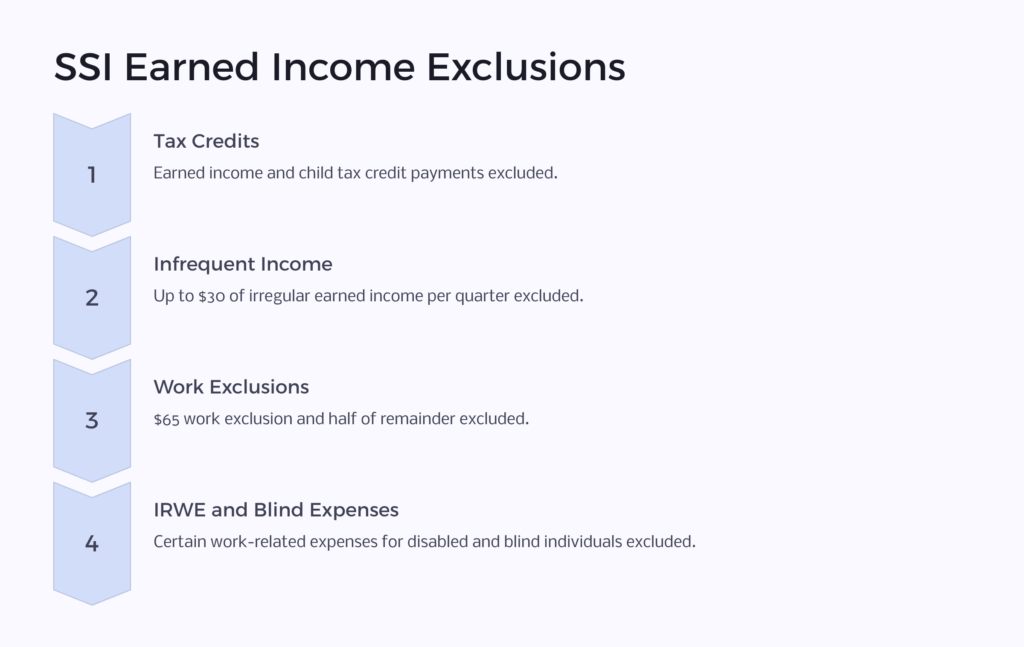

SSI Earned Income Exclusions

In addition to the work-incentive provisions already mentioned, certain types of earned income are excluded from counting against the SSI income limit. Some of the exclusions are earned income tax credit payments, child tax credit payments, and $30 of infrequent or irregular earned income. There is also a $65-a-month earned income exclusion and exclusion of half of the remainder and a $20 general exclusion if you don’t have unearned income. The exclusions are applied in the order shown below.

Order in Which Exclusions Are Applied

Earned income exclusions are applied in the following order.

- Earned income tax credit payments and child tax credit payments.

- Up to $30 of earned income in a calendar quarter if it is infrequent or irregular.

- The general exclusion of $20, if you do not have unearned income.

- The $65 work exclusion

- Earned income used to pay the Impairment-Related Work Expenses of a disabled, non-blind person.

- One half of the remainder after all the earned income exclusions.

- Earned income used to pay blind work expenses.

- Earned income used to fulfill an approved Plan to Achieve Self-Support.

If your earned income exclusions exceed your earned income, the unused exclusions cannot be applied to unearned income and cannot be carried forward for use in a future month.

Getting Back on SSI with Expedited Reinstatement

If your SSI benefits are terminated because of your work earnings and you become disabled from the same condition for which you originally received SSI and your recurrent disability begins within five years of the date your SSI ended, the Social Security Administration will expedite reinstatement of your benefits so that you can receive SSI payments while your claim is undergoing a disability review.

These provisional benefits include a Federal SSI payment that may be accompanied by Medicaid eligibility. They do not include state supplements. The provisional payments can continue for up to six months while your SSI and disability claim is pending. If the Social Security Administration decides that you are not eligible for benefits, usually they do not ask you to repay the provisional benefits.

Wage Reporting

Some earned income does not count toward the SSI income limits. However, even if income is excluded, the amount and source of the excluded income have to be reported and verified. That means that you will be asked to provide proof of the amount of your earned income and when it was paid as well as proof of any Impairment-Related Work Expenses and expenditures for your Plan to Achieve Self-Support. If you are participating in the Ticket to Work Program, you should also report your earnings to the vocational counselor who is assisting you.

Employee gross wages—the amount you earn before taxes and other deductions–must be reported to the Social Security Administration by the tenth day of the month following the month the wages were earned. For example, if you receive earnings in September, you must report the amount, the date, and the source by October 10. Failure to do so can result in underpayments, overpayments, and penalties. You must also report if you start or stop work, including starting or stopping a second or third job, or changing duties. If you are self-employed the Social Security Administration will provide you with instructions on how to report changes in your net income and net income estimates.

The Social Security Administration has devised a telephone system to make reporting wages quick and easy. If you qualify to use telephone reporting, you must report your previous month’s wages by the sixth of the month, not the tenth. The Social Security Administration will give you worksheets and instructions for reporting by phone.

Whose Wages Must Be Reported and Who Can Report Wages

You or your representative payee is responsible for reporting your wages and net earnings from self-employment and for reporting the earnings of anyone who deems income to you. The “deemors” can also report their own earnings. At each report, the caller will need to provide his or her Social Security number and name as it appears on his or her Social Security card and the Social Security number of the person receiving SSI.

In summary, in answer to your question about how to get SSI benefits and work, SSI law has included many provisions to help you work to your capacity and either continue to get SSI or to become financially independent.

Impairment-Related Work Expenses for Non-Blind Disabled Workers

If you have Impairment-Related Work Expenses (IRWEs), those expenses can be used to reduce the amount of the countable income Social Security uses in your SSI payment calculation, so that effectively SSI covers those expenses.

The Social Security Administration may reduce your countable earned income by the amount of your out-of-pocket expenses for such expenses as medicine; medical services, supplies, and devices; and service animals. Other expenses that might be deducted from your earned income are attendant-care services to prepare you for work, to attend you while at work, or to help you get to and from work. Other possible Impairment-Related Work Expenses can include special transportation to get to work and handicap modification of your home, car, or van if they are needed for you to work.

Reimbursed expenses cannot be deducted from your earnings. Additionally, the expenses must be needed in order to work and they must be related to your disabling impairment. For example, if you have work expenses of union dues, health insurance, and a lift van to get you to work, the expenses for the lift van could be used to reduce your work earnings, but the union dues and insurance could not because they are not impairment-related.

Usually, it does not matter that you also use the item during non-work hours as long as it is also needed to work. For example, you would need medication and a wheelchair even if you were not working; but because they are also needed for work, your out-of-pocket cost for these items can be used to reduce your countable earnings.

Work Expense Exclusions for the Blind

Blind work expenses include all the SSI Impairment-Related Work Expenses that non-blind, disabled SSI recipients qualify for. In addition, a blind individual’s work earnings will be reduced by all expenses related to working, whether or not they are related to blindness. Some of these exclusions are licenses, fees, payroll taxes, and meals eaten during work hours, and work-related equipment or services.

Social Security Disability Is Different

It is important to remember that the earned income exclusions discussed in this article relate to your SSI eligibility and how to get SSI in a larger amount. If you also receive Social Security Disability (SSDI) benefits, a different set of work incentives apply to your Social Security claim.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.