Social Security Disability Insurance (SSDI) provides crucial financial support to millions of Americans who can no longer work due to severe, long-term disabilities. Yet one question often arises: Is SSDI considered government assistance?

The answer is nuanced. While SSDI is administered by the federal government through the Social Security Administration (SSA), it is not a welfare program in the traditional sense. Instead, it is an earned benefit—workers and employers pay into the system through payroll taxes, and eligibility is based on work history, medical disability, and having paid Social Security taxes.

What is Social Security Disability Insurance (SSDI)?

SSDI is a federal insurance program created under Title II of the Social Security Act. It provides monthly benefits to individuals who have a qualifying medical disability that prevents substantial gainful activity (SGA) and who have accumulated enough work credits by paying Federal Insurance Contributions Act (FICA) taxes. In essence, SSDI acts much like an insurance policy. Workers contribute during their careers, and self employment income also counts toward work credits for SSDI eligibility. If they later become disabled, they may ‘draw’ from the system. In some cases, a family member, such as a spouse or parent, may qualify a dependent for SSDI based on their work record.

SSDI vs. Government Assistance (Welfare)

To understand whether SSDI counts as government assistance, it helps to distinguish between social insurance programs and public assistance programs.

Social Insurance Programs:

- Funded through payroll contributions.

- Benefits are ‘earned’ by participants.

- Examples: Social Security retirement, Medicare, SSDI.

Public Assistance Programs:

- Funded through general tax revenues.

- Based on financial need, not work history. Eligibility for these programs is determined by gross income and countable income limits, which set thresholds for qualifying based on total income and specific earnings criteria.

- Examples: Supplemental Security Income (SSI), Temporary Assistance for Needy Families (TANF), Supplemental Nutrition Assistance Program (SNAP).

Common Confusion: SSDI vs. Supplemental Security Income (SSI)

One major source of confusion is the similarity between SSDI and SSI:

- SSDI: Work-based insurance benefit. Not means-tested.

- SSI: Need-based assistance for low-income individuals with disabilities or limited resources.

While both programs are managed by the SSA and serve disabled individuals, only SSI is considered traditional government assistance (welfare).

SSI benefits are given due to limited income and financial resources. SSI recipients receive monthly cash payments, which are funded by a federal SSI payment and may be supplemented by state payments. The maximum monthly SSI payment is set by the federal government and can vary based on living arrangements and other factors.

Eligibility for SSI is based on limited income, financial resources, and may be reduced by support such as free shelter or food. Children with severe functional limitations or severe disabilities may qualify for SSI, and disabled recipients can continue to receive benefits even if they work, under certain conditions.

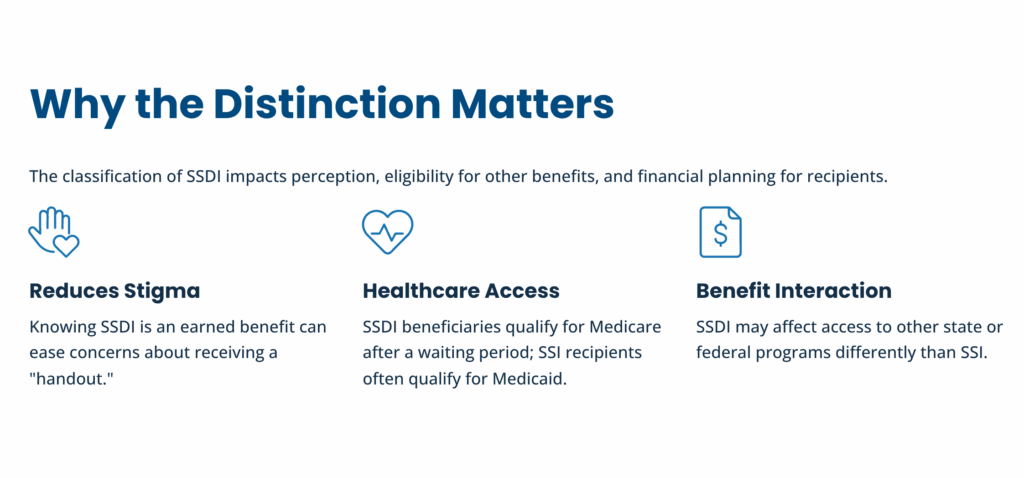

Why the Distinction Matters

The classification of SSDI affects perception, eligibility for other benefits, and financial planning. Recipients often worry about stigma, but knowing SSDI is an earned benefit can ease concerns. SSDI may affect access to state or federal programs differently than SSI, and beneficiaries also qualify for Medicare after a waiting period.

SSDI recipients become eligible for health care coverage through Medicare after a five-month waiting period, and may also be eligible for retroactive benefits depending on the disability onset date. SSI recipients often qualify for Medicaid eligibility, which provides health care coverage for low-income individuals.

SSDI Funding by the Social Security Administration

The Federal Insurance Contributions Act (FICA) taxes fund SSDI. Both employers and employees contribute: 6.2% from the employee’s paycheck and a 6.2% employer match. Social Security taxes are collected from both employees and employers to fund SSDI and other benefits. Only individuals with sufficient Social Security covered employment, meaning they have earned enough work credits through jobs covered by Social Security—are eligible for SSDI. The Social Security Administration uses these funds to pay benefits, and the SSDI benefit amount is based on the individual’s earnings history. These contributions support both retirement and disability insurance programs. Because recipients have already paid into the system, SSDI is legally and financially an insurance payout, not a welfare benefit.

Real-Life Implications of Disability Benefits

For Recipients:

- No need to prove financial hardship (unlike SSI or SNAP).

- Entitlement is based on disability status and work credits.

- Individuals who meet the work and disability requirements can receive SSDI benefits.

- Monthly payments provide stability and dignity.

For Public Understanding: Many Americans lump all federal benefits into the category of ‘government handouts.’ This misunderstanding can create stigma, even though SSDI is as much an earned right as Social Security retirement benefits.

Receiving benefits through SSDI is based on prior contributions and disability status, and disability beneficiaries are entitled to receive benefits as a matter of right.

Criticisms and Challenges

While SSDI is not government assistance in the welfare sense, it does face challenges such as funding strain, approval delays, and persistent stigma about ‘deservingness.’ The SSDI application process can be lengthy and complex, contributing to these approval delays. There are also special rules designed to help beneficiaries return to work without losing their benefits.

Additionally, SSDI does not provide benefits for partial disability—only for those with total disability as defined by the SSA. Administrative costs are another concern, as they impact the program’s long-term sustainability. These highlight the importance of clarifying SSDI’s role as a social insurance program.

Conclusion

So, is SSDI considered government assistance? The short answer is no—not in the traditional welfare sense.

While SSDI is a federal program, it is an earned benefit funded by payroll contributions. Recipients qualify because of their work history and disability, not financial need. This distinction matters for reducing stigma, protecting beneficiary rights, and shaping public understanding. SSDI recipients should feel assured: they are not receiving a handout, but rather accessing an insurance benefit they worked and paid for throughout their careers.

Here at Benefits.com, we are here to help you navigate the process and receive the benefits you deserve! Begin today by taking our free eligibility quiz.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.