Self-sufficient adults need money management skills. These articles are about the very basics of money management, and would apply to anyone including young people who are just beginning to be responsible for themselves, someone who is new to the United States currency and working within our banking system, or someone who has not had to manage on a fixed income before, such as those receiving social security disability benefits.

You may have a firm grasp of these skills already. Becoming disabled later in life requires acceptance of many changes, including a change in mindset and in your financial plans going forward. Money may now need to be allocated for making adjustments to your home, and budgeting needs to include medications and regular doctor visits or treatments. It is important to incorporate these changes into your ongoing budgeting plans and to acquire sound financial habits for your future.

Financial wellness is a hot topic that includes not only understanding how to manage money but also how to make wise financial decisions that can improve your overall well- being. Your disability benefit, just like other types of money, checks, or payments comes with little guidance on how best to manage it. Figuring out how to maximize this benefit in your life requires information and skills. Whether you have handled finances for yourself or your family for years or have recently taken charge of your money, here is a quick overview of basic money management to guide your habits, actions, and choices.

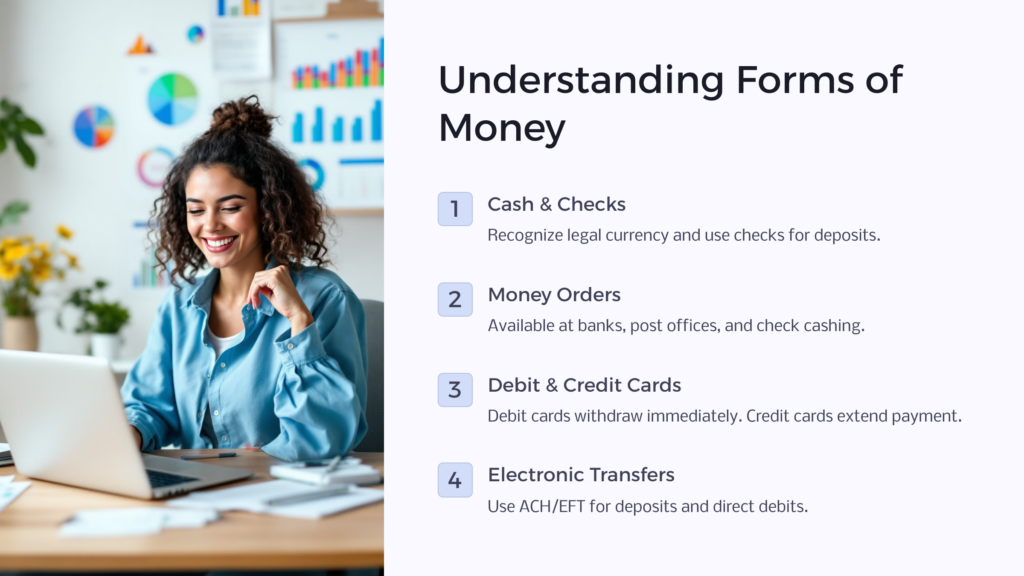

Skill # 1:Understanding Forms of Money

Cash is probably the easiest form of money to recognize or spend. If you are relatively new to the United States, or are new to handling money, you should know that our legal currency includes $1, $2, $5, $10, $20, $50 and $100 bills and the 1¢, 5¢, 25¢, 50¢, and one-dollar coins. You probably haven’t seen the $2 bill or fifty cents and dollar coins as often but they are still circulating as legal tender. Of course, any amount of money can be written in the form of a check to be deposited as money in your bank account or cashed for bills and coins. And any amount of money (cash, checks, or payments) can also be deposited in a bank account either in person, at an ATM or electronically. Some people have gold or silver coins that are worth a certain amount (that can vary daily) and considered legal tender (in some states) but these coins must be exchanged for currency in order to be used for purchases.

While not considered cash, other items that may be used for purchases or exchange include:

Money Orders (available at various businesses, banks, the post office or check cashing establishments),

Certified Checks (signed by you but the bank certifies that you have the money in an account to cover the check),

Cashier’s Checks (issued directly from the bank and considered more secure than a certified check),

Traveler’s Checks (most often used as a safe alternative to cash or credit cards when traveling outside the US but can also be used in the US),

Make sure you understand the circumstances of use for each type of card. For example, Credit Cards, debit cards, store-credit cards, and gift cards.There are also cards that appear to be credit card (with logos from VISA, American Express, and MasterCard) that you load by using cash. Minus a small activation fee, these cards can then be used as debit cards up to the amount of cash you put in.

Debit cards immediately remove the amount from your bank account while credit cards extend the payment until the monthly due date and charge interest if the amount is not paid in full.

Store-credit and gift cards usually have rules regarding their usage. If you are unsure, ask at the store if you can receive change in cash from a purchase if it is less than the total amount on the card or if the amount left remains on the card for future purchases.

Electronic transfers of money are used extensively now through such systems as ACH (Automated Clearing House) and EFT (Electronic Funds Transfer). Both terms can be used interchangeably and refer to a transfer of funds from one bank account to another electronically. For example, with credit and debit cards banks verify payment through these systems at the point of purchase. As of March 2013, all SSDI checks are deposited electronically.

ACH/EFT can also be used for electronic deposits, direct debits or deductions, as well as direct deposits.For example, you may set up to have one or more of your regularly-scheduled monthly bills automatically deducted from your account and sent to the vendor through an ACH/EFT.These systems can also be used to transfer money from your bank account to purchase items on a debit or credit card set it up in advance with a specific vendor (such as Amazon) to use for each transaction. There are also specific payment systems you can use so that you don’t have to set up a unique account with every online vendor. PayPal and Google Wallet are examples of this.

Confused about keeping all of these forms of money straight? Even if you receive your benefit check electronically, some people only feel comfortable using cash or a combination of checks and cash to keep track of daily purchases or paying bills. Your level of comfort in using the various alternative forms of money listed here should be tied to your understanding of the risks, benefits, and even costs associated with each them.

Skill # 2: Setting a Budget for Spending and Saving

Here is the one skill related to money management that can make or break individual or family finances: Budgeting. When people don’t know where all their money goes or are upset that they don’t have enough money to take care of their obligations, the fault often lies in ignoring the budget process, which includes spending and saving.

There is probably more information on the Internet and in finance books about creating a budget than any other money-related topic. Simply put, a budget is a record of money coming in and money spent. You can create a budget for each month, each week, each day or even over a year or longer. The purpose of a budget is to give you peace of mind that you have money to pay for what you need. When a budget works, you can feel more secure in knowing that you can take care of yourself and plan for the future instead of worrying constantly about finances.

First, you have to have an accurate picture of the money you have and how you spend it. Here are two simple ways that might work for you if you are new to budgeting or if your current plan is not working.

- Keep a daily log by writing down every item you purchase and any bills that are paid by cash, check, or electronic transfer. Most people are surprised after they collect this information for a few weeks or months. You can estimate what you spend on food, for example, by keeping track of grocery receipts. But once you write down each trip to a coffee shop or every pizza delivery, you begin to get a better idea of what you spend on food and drink. The longer you keep a log, the better you can understand and anticipate upcoming expenses.For example, in two weeks or even a month, you may not spend money on clothing. But at some point you or someone in your family may need new shoes or a jacket that you have to buy. For one month it might look like you don’t need to budget much for clothing but over time, you will. The same thing can happen to utility bills that can fluctuate wildly depending on the weather or car expenses that can ruin your carefully planned budget if you get a flat tire or need a repair. A simple daily log can be valuable information in figuring out what expenses you can expect, bearing in mind that unplanned expenses or emergencies can always be on the horizon.

- Set up a monthly budget that you plan to follow. This means writing down all anticipated expenses, either the exact amounts or estimates into categories such as rent, utilities, food, personal care, health care, transportation, recreation, and others. For some categories, such as rent, you know exactly what the amount is. For others, you can estimate an amount, either based on analysis of your daily log or past experience. Keep in mind that on average, housing is 25-35% of your total, with 10-15% for each of the categories of utilities, food, personal care, and transportation.

Of course, your percentages may vary greatly depending on your personal needs in each of these categories. Your health care needs may also be a bigger expense than most people although there are several programs available in communities and states to help with costs related to your health and disability. Review the monthly budget amounts you have written down next to each category and under the figure put the exact amount spent in that category until the end of the month. At the end of the month, review how close your estimates came to covering your expenses. Make adjustments for amounts budgeted for the upcoming month and repeat the review for at least two month.

Did you notice that Skill # 2 is Setting a Budget for Spending and Saving? The easy part is coming up with what you are spending. Sometimes you might feel you have little control over what you have to spend for something, such as housing or your monthly transportation costs—or do you?Here is where you can really get creative by learning how to spend less and save more. If you’re thinking that is impossible in your situation, maybe these three stories can change your mind.

Janis in Illinois

I used to spend whatever money I had each month until it ran out. I soon learned that I had to do something because I was running out sooner than I had planned. So I turned into what some people might call an extreme budgeter–and that is fine with me. Each week, I try to make it a personal challenge to find ways to cut my expenses. My favorite ways are in the food category. Since November, I have been able to cut my food bill by 10% each month. I started by setting up a monthly menu, including breakfasts, lunches, dinners, and snacks. Yes, that took some time. But once I had the menus set, I knew exactly what to buy at the store instead of guessing what I might want to eat once I was in front of all the temptations at the grocery store. This one little tip made it possible for me to buy items like beans, rice, pasta, cheese, and eggs in bulk and use up things before they were spoiled and no one would eat them. Have there been days when I wasn’t thrilled with my menu choices? Oh yeah! But I am getting better at it each month and enjoying the entire process more. I’m very proud of all the money I have cut from my food spending without starving my family.

Manny in Florida

My utility bills were getting out of sight–especially during the hot summers here in Miami. So I decided to do two things: First, I told my kids we were going to play detective and try to spot places where the air conditioning was leaking outside and extra heat was coming through to the inside. We used weather stripping to cover some of the holes and spaces around doors and windows and pulled the blinds shut in rooms that were flooded with light (and heat) during the day as much as possible. The best part about this was that everyone became more interested in “keeping out the heat”– not just me.Next, we started adjusting the temperature to make it a little bit warmer, a little less air-conditioned in the house–one degree at a time. We found out that we could easily tolerate our house being several degrees warmer than we thought we could, even at night. After six months, we had saved more than $200 on our utility bill that really helped our budget.

Ross in Colorado

I had always had my own place to live since I left school twenty years ago. But after hurting my back disabled me, I could no longer keep my job or keep up my large apartment. So I talked to everyone in my family and found that one of my aunts was willing to let me come and live with her to help share expenses. I thought it would drive me crazy to have another person in the house with me at all times, but it has worked out surprisingly well. We respect each other’s privacy and have actually shared some fun times eating together and watching movies together on TV. I would never have imagined myself living with one of my relatives but when circumstances change, you have to be flexible and open-minded. This arrangement wouldn’t work for everybody but we have found a way to make it work for both of us.

These people and millions more have found ways to cut expenses and save money. Stories of people finding unique ways to stick to or reduce their spending can be found on the Internet, in your neighborhood, or even in your own circle of friends and family. Don’t be afraid to bring up the topic so you can share your own ideas and learn from others.You are in the majority of Americans if you are watching your expenses and trying to find ways to spend less and save more.

And keep reading because in Part Two of Money Management Skills we are going to tackle additional areas of personal finance that can help you make the most of your benefits.

Once you have the basics of money and budgeting, you are ready to tackle a few more advanced skills to build your expertise.Here we will focus on credit and debt, planning for emergencies, adding to your income, and continually improving your finance knowledge and skills. Ready?

Skill # 3: Handling Credit and Debt

Some information about the use of credit cards was covered in the section on understanding forms of money. But here we are focused more on credit itself– as the ability to purchase goods and services now with a promise to pay in the future.

Some information about the use of credit cards was covered in the section on understanding forms of money. But here we are focused more on credit itself– as the ability to purchase goods and services now with a promise to pay in the future.

Obviously this involves some level of trust. Why would anyone repair your broken tooth or let you take a pair of shoes home from the mall today if you just tell them you will pay them in a week or month or even later? The answer is that almost anyone will if you have good credit. That sounds like a powerful item to have, and it is. But creating and maintaining good credit takes constant awareness and responsible practices with your finances.

Remember back in school where you were graded on spelling tests or science projects all resulting in a final grade for a class that when all grades are calculated resulted in a cumulative GPA (grade point average)? A credit score is just like that grade point average. Everyone who has any history of purchases at all on credit, from buying a car, paying electric bills, or taking out a student loan has a credit score. The scores range from 280 (not good at all) to 850 (excellent!!!). As you might guess, your credit score changes throughout life depending on how you use credit and pay off your debts.

Here is where it gets a little complicated. Every time you pay for something using a credit card or a loan, such as a car loan, or have an open account (such as utilities), you add information (like a new grade) to your credit history. If you are late or skip a

ayment that reflects negatively on your history and if you pay consistently on time it is reported as a positive. Any bankruptcies or judgments (such as child support obligations) reported in public records also figure into your information.

Your credit history is then put together in a report by three different credit bureaus: Experian, Equifax, and TransUnion. By law, you are entitled every 12 months to one free report from each of these organizations and should take advantage of that to ensure your credit history is accurate. You can gain access to these reports by going to AnnualCreditReport.com or by calling 1-877-322-8228. The companies report credit activity slightly differently but they are generally within a few points of one another.

Let’s say you want to rent an apartment. Your potential landlord can ask for your personal information to check your credit history. So, too, might a government agency, a retailer if you are applying for a store credit card, or anyone else who is considering granting you credit.

Remember, you, too, can access your credit report and if you do, you can easily see what information others will see. All credit reports include your Social Security number, all previous addresses and telephone numbers, birthdate, and employment history. Of course your history of payments (or lack of payments) on your accounts as well as your applications for and use of credit are included. Such information as your race or marital status cannot be included nor can medical information, bankruptcies older than 10 years or debts older than 7 years. The agency or landlord deciding to grant you credit or to risk renting property to you then uses the report, including the numerical score to make a decision about you. All inquiries about your credit history are also included in the report.

As you can see, your credit history is very important going forward in your plan to improve your financial situation. If your credit history is poor, then you need to work on repairing it by paying all your bills on time. If there is a mistake in your credit report, you need to contact the credit bureau to get it straightened out. Again, you can access your own information free at:

AnnualCreditReport.com or by calling 1-877-322-8228

Debt is money owed, usually with some agreement about repayment time and amount. When you don’t have enough money to pay for your bills or the things you need and want, credit can be a backup source of funding. But financial advisors agree that credit should be used sparingly and generally for big-ticket items such as a car, mortgage, or even student loans, not for groceries, monthly bills, or nonessentials. Any balance on a debt that is not paid on time, especially credit card bills that you either don’t pay the entire amount or skip a month, accumulates interest. If you are using credit to pay most of your bills each month because your debt is always greater than the money you have available, you are going to accumulate large fees that can completely crush your ability to ever dig out of debt.

For example, if your credit card company charges 15.25% interest on unpaid balances, a $100 item will cost you $115.25, and if you don’t pay in full the following month, the $100 item will now cost you $132.83. You can see how the more debt you owe, the more difficult it is for you to keep up with your monthly budget and save money for something you really need or for emergencies.

Skill # 4: Planning For Emergencies

What would you do if you were suddenly confronted with a $400 repair bill on your car you need to get to the store or the doctor? Or you had to fly to another part of the country to help a sick relative? Of course you could use a credit card for these expenses, if you have one. But as we just discussed, having money saved for unplanned events or emergencies is one of the best ways to avoid debt and meet your goals of financial wellness.

Having $400 or even $200 in a savings or emergency fund may sound impossible. Few people are able to save that much money each month. But setting up a plan to save something, even as small as $5 a week or $10 a month, can set you on the path to establishing that fund. And here is a little secret that might encourage you: People who begin to save even a little bit, are motivated to examine their budget to find even more ways to save money. There are thousands of people who are trying to increase their savings and create a fund so that when a money emergency happens (and they happen to all of us) you have a fund in place that you can access easily to take care of it.

How much should people plan to have in an emergency fund? The answer is as much as you can. Sure it would be great to have enough money to pay all your bills for at least 3 months. But every little bit helps and adds up. If you don’t already have one, commit today to start one just to put you on the path towards financial success. Every dollar you commit to an emergency fund brings you one dollar closer to managing your money and life successfully.

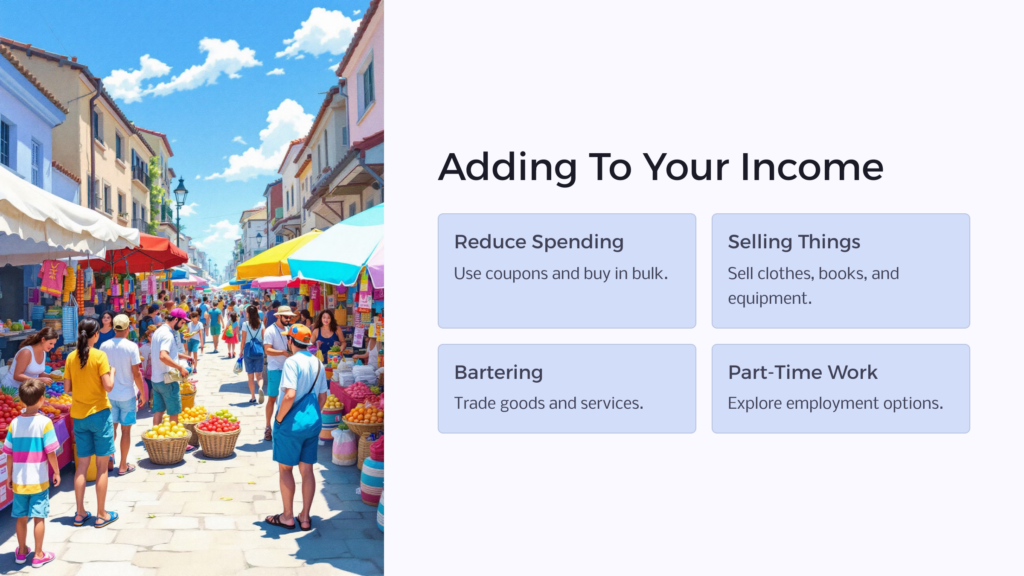

Skill # 5: Adding To Your Income

Once you set up a budget, you have to carefully watch your spending to make sure you don’t spend more than you have each month.At some point, you might wonder if there is some way you can boost your income beyond your disability payment.Here are some ways you might want to investigate as possibilities for adding income to your monthly or yearly budget to help with expenses or setting up a healthy emergency fund.

Reduce spending

Are there items in your budget that can be eliminated or the amount spent lowered? For example, can you save money on food by paying attention to specials, buying only items that are on sale, using coupons, or buying in bulk? Could you share some meals with others that would reduce waste or help stretch your food dollars? It takes some time to organize your grocery shopping and menu planning to cut your food budget but the rewards can be significant. There are blogs on the Internet completely devoted to saving money on grocery shopping as well as articles that can help you think about ways to reduce spending on everything you need to pay for that could make sense for you. Here are a few you might like to read:

Selling things

It has been said many times that Americans all have too much stuff! If that applies to you, maybe you can find a way to sell clothes, books, DVDs, games, toys, equipment and other items to add a little bit to your income. There are many different ways you can sell items in person or on the Internet from having or being part of a garage sale to posting items for sale on eBay or Craigslist. Some people enjoy hunting or collecting unwanted items from others that they can resell for cash or gift cards. In fact, there are entire websites devoted to helping you figure out how best to sell things. Take a look at these for some ideas to get you started:

Bartering

Bartering is trading goods and services for other goods or services without exchanging money. It can be as simple as trading babysitting for lawn service or as complicated as setting up a bartering bank where a group of people come together to exchange their talents, skills, or items. Because bartering is usually a personal transaction, it’s important that you and the person you are bartering with understand the expectations and critical details of the trade. People have been informally bartering for years. Perhaps this method might help you free up additional income each month in your budget. A beginning guide to some aspects of bartering is below:

Part or Full Time Employment

Wait! Can a person have a job and continue to collect disability benefits? Isn’t the fact that you have a disability the reason you can’t work?

Yes, you can work and continue to collect disability benefits. There are definitely rules regarding the amount you can earn per month, reporting to Social Security your intention to seek employment or actual employment, and receiving assistance while you are training for a new career or job. This is one of the most misunderstood aspects of being a disability beneficiary and deserves more than the short space devoted to the topic here. The link to information from SSA about working while receiving disability benefits is below. And stay tuned to more information here that can help you explore this exciting opportunity for you to add to your income.

Skill # 6: Always Improving Your Money Management Skills

Your ability to make knowledgeable decisions about how best to manage your financial resources can be one of the most valuable resources you have to manage your disability and improve the quality of your life. No matter how confident you might be about your money management skills, the world of finance is constantly changing. To keep up, you can pay close attention to financial news in the media, read books or articles on the subject, and talk to people you know about their relationship to money and the tips they use to be financially successful. Yes, money is one of those touchy subjects that many people are not comfortable discussing. But without disclosing specifics, you can bring up the idea of sharing money tips or ask others for advice on how to take care of financial issues, topics that most people can participate in and learn from.

If you are really serious about learning more, you can also take in-person classes on basic money management or finance through community organizations. Also, there are several excellent and free online courses to boost your money IQ such as the ones listed here:

Smart About Money (The National Endowment for Financial Education) https://www.nefe.org/initiatives/smart-about-money.aspx

Better Money Habits (Bank of America and Khan Academy) https://about.bankofamerica.com/en/making-an-impact/financial-education-resources-advice

Managing My Money (Future Learn)

Money Management: Head Matters (CollegeInColorado.org)

In addition, several beginning and advanced classes on financial topics are offered through Udemy

Whatever works best for you, make sure you work on improving your money skills frequently as part of your plan to move beyond where you are today towards a better future.

By Jackie Booth, Ph.D.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.