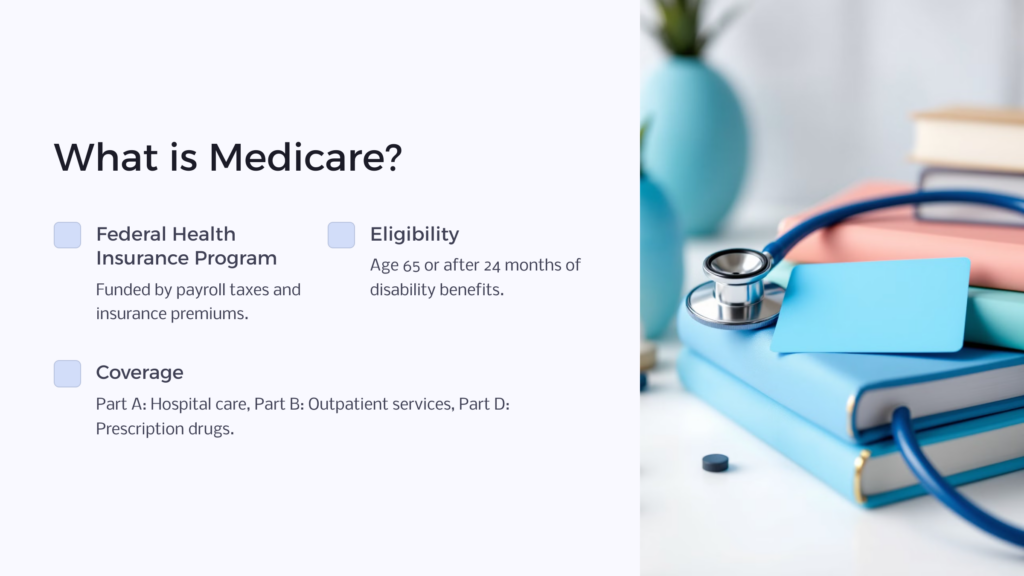

What is Medicare?

Medicare is a federal health insurance program paid for by payroll taxes and insurance premiums. The FICA tax withheld from your paychecks and matched by your employer or the self-employment tax you pay as a self-employed person includes a tax to fund Part A Medicare, which you will become eligible for at age sixty-five or after twenty-four months of entitlement to one of Social Security’s three kinds of disability benefits. A spouse age sixty-five who is receiving spouse’s benefits only can receive Medicare Part A without premium based on his or her spouse’s work.

A very small percentage of people work in occupations or for employers not covered by Social Security. Those individuals pay only Medi-tax to secure Part A Medicare insurance. If no taxes have been paid for Medicare Part A, it is possible to purchase Part A with the payment of premiums when you reach age sixty-five.

Part A Medicare covers inpatient hospital care, hospice care, and some other medical services. The remainder of Medicare—Part B for doctors and most outpatient services and Part D for prescription medication—is optional and is funded by monthly premiums paid when eligibility starts, that is, after twenty-four months of disability benefits from the Social Security Insurance program or at age sixty-five.

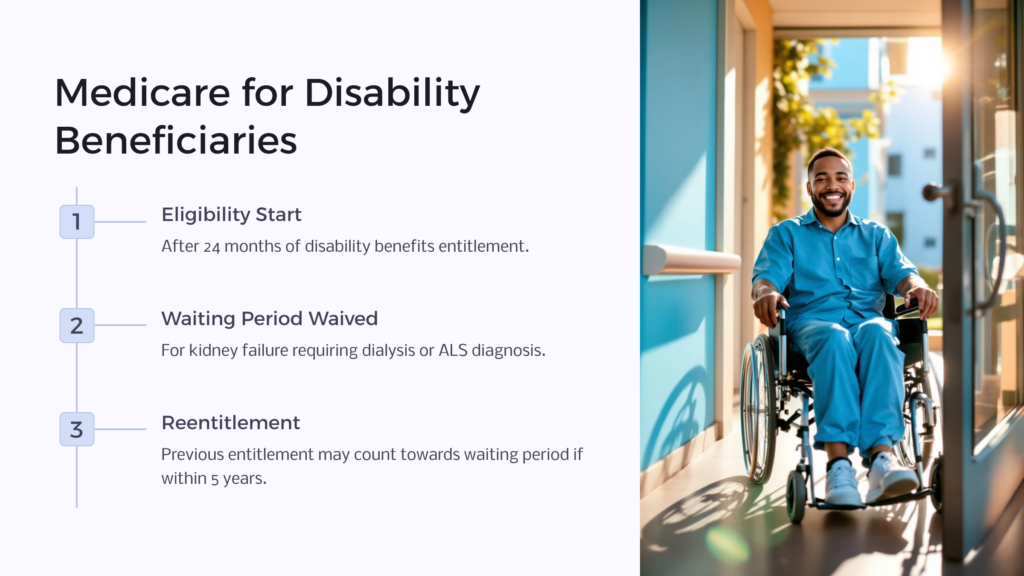

Medicare for Social Security Disability Beneficiaries

If you are eligible for Social Security Disability on your own earnings record or are eligible for disabled surviving spouses or disabled surviving divorced spouses benefits, you will become eligible for Medicare after you have been entitled to benefits for twenty-four months including any months of back benefits paid upon your approval. Because these benefits begin after five full months of disability, Medicare starts in the thirtieth calendar month of your disability as established by the Social Security Administration. Childhood Disability Benefits (CDB) on a parent’s earnings record have no waiting period; therefore, Medicare entitlement for CDB beneficiaries starts in the twenty-fifth month of disability.

When the Medicare Waiting Period is Waived

If you are insured for Medicare through payroll or self-employment taxes, no Medicare waiting period applies if you have kidney failure requiring regular dialysis or a kidney transplant or if you have amyotrophic lateral sclerosis, also known as ALS or Lou Gehrig’s Disease. If you qualify for Medicare without a waiting period due to those diagnoses, you can receive Medicare insurance without stopping work and without receiving Social Security benefits. In other words, you can keep working if you are able and still get the medical treatment needed for these chronic progressive diseases.

When a person recovers and stops receiving Social Security Disability benefits and again becomes disabled from the same or a related condition, months from the prior period of entitlement will count toward the twenty-four-month Medicare waiting period if the established disability date for the current claim is within five years of prior claim closing. Disabled surviving spouses and disabled surviving divorced spouses get the same break if they become disabled again within seven years of prior termination. This means that if a person was entitled to Medicare previously there would be no new waiting period or the period would be less than twenty-four months.

Interestingly, a person’s current type of Social Security disability entitlement does not have to be the same as the prior entitlement for this rule to apply. For example, a person could be eligible for disabled widows benefits, be terminated due to work, and later become entitled to disability on his or her own earnings record and still have months of eligibility from the prior claim count toward the Medicare waiting period.

How to Pay for Medicare

Medicare consists of three parts, which provide three different coverages. As discussed, Medicare Part A, which covers hospitals, hospice, and some other benefits, usually does not require a premium payment because usually it has been paid for through taxation. Both Medicare Part B, which is for doctors and most outpatient services, and Medicare Part D, which is for prescription medication, require payment of a monthly premium.

If you are receiving Social Security benefits when your Medicare entitlement begins, the premium for Part B Medicare will be withheld from your benefits. You will be notified of your entitlement and collection of premiums will begin automatically unless you refuse the Part B coverage. (See “When You Should Enroll for Parts B and D Medicare at the First Opportunity” later on in this article.) If you are age sixty-five and have not yet started to receive Social Security because you are not disabled and have not applied for reduced early Social Security Retirement, you will have to file an application for Medicare and pay your premiums quarterly by mail, online at www.medicare.gov, or by direct automatic debit from your bank account.

When You Should Enroll for Parts B and D Medicare at the First Opportunity

Your initial enrollment period for Medicare Parts B and D is seven months long—three months before your twenty-fifth month of disability entitlement or before the month you turn age sixty-five through three months after the month you qualify.

If you do not enroll for Medicare Part B for doctors and out-patient medical services during your initial enrollment period, in many cases you will have a late enrollment penalty, which will permanently increase your Part B premiums. If you want to keep employer-sponsored health insurance and work for a company with less than twenty employees, then you should enroll in Medicare Part B and Medicare will be the first payer on any of your claims. If you are employed by a larger company, check with the benefits department to find out whether your health insurance policy through work requires you to apply for Medicare Part B and/or Part D as a condition of continued coverage. If it does not and it provides coverage comparable to Medicare including comparable or better prescription coverage, you can defer applying for Medicare until you no longer have the company insurance. At the time, you will be given a short personal enrollment period.

If you decide not to apply for Medicare Part B during your seven-month initial enrollment period and you do not have another insurance that will make you eligible for you a personal Medicare enrollment period at a later date, you will be able to enroll later only during the open enrollment period, January 1 through March 31 and the Part B insurance coverage will not begin until the following July. Additionally, a late enrollment penalty will permanently raise your premiums above the base rate that would apply if you had initially enrolled. The longer the time between your initial enrollment period and when you enroll, the higher the penalty.

Similarly, if you do not enroll in Medicare Part D for prescription medication and do not have other “credible” (comparable) prescription coverage or are not enrolled in certain Medicare-related plans offering prescription coverage for any period of sixty-three days or longer after your initial enrollment period, later, when you need and want prescription insurance through Medicare, your Part D premiums will be higher due to a late enrollment penalty and you will be allowed to enroll only during an open enrollment period, January 1 through March 31 of each year.

Because Medicare regulations related to delaying enrollment in Part B and Part D Medicare are detailed and specific, Disability Advisor recommends that you seek guidance from www.medicare.gov, your local Social Security office, and/or an informed insurance agent before making these important enrollment decisions.

What is Medicaid?

Medicaid is a medical insurance program, separate and different from Medicare. There are many ways to qualify for Medicaid, but eligibility for Social Security Disability is not one of them.

Medicaid is a needs-based health insurance program that requires either no premium or a small premium. It requires either no deductible or co-pays for services or only a small copay and usually includes prescription medication coverage. Medicaid is funded by general tax revenues collected by the federal government and the individual states. Because states participate in funding and administering Medicaid, the financial criteria for Medicaid eligibility, the services Medicaid covers, and who demographically will be eligible for Medicaid vary from state to state.

Even within a state, the exact income and resource (asset) limits for eligibility vary. For example, the income and asset limits for an elder applying for Medicaid to pay for assisted living or memory care is different from that of someone else applying to have Medicaid for doctors and hospital coverage.

Except for Medicaid eligibility through entitlement to Supplemental Security Income (SSI), application for Medicaid insurance has to be made to your state through your closest state or county social services office.

Medicaid and Supplemental Security Income (SSI)

If you are approved for Supplemental Security Income (SSI), you will automatically be eligible for Medicaid. Medicaid coverage that is based on SSI eligibility covers medical services and prescription medication. It does not require premium payments and has no co-pays or deductibles. Medicaid eligibility continues for any month in which at least one dollar of SSI is payable. Medicaid eligibility based on SSI eligibility results in the Medicaid program paying your Medicare premium. Note that if a person’s SSI eligibility is periodically interrupted due to spikes in countable family income or excess resources, Medicaid coverage and Medicare premium payment will be interrupted as well.

Help with Medicare Premiums

As stated above, if you are entitled to both Medicaid based on SSI eligibility and Medicare, Medicaid will pay your Medicare premiums for you. If you are eligible for Medicaid, but not based on SSI eligibility and you have limited income, Medicaid may pay the Medicare premium. Other programs offer financial assistance to individuals who don’t qualify for Medicaid but who have limited income and assets. To find out more, go to www.medicare.gov, click on “Your Medicare Costs,” then on “Get Help Paying Costs,” and finally on “PACE,” where you will find a description of some of the assistance programs.

Will my benefits increase because I became disabled while collecting early Social Security Retirement benefits?

If you become disabled while receiving Social Security early retirement benefits, whether or not you receive an increase in benefits depends on when you became disabled. Social Security does not pay disability benefits for the first five full calendar months of disability, so you would not get an increase during those months. You would receive an increase in the sixth month if the sixth month is before your Normal Retirement month.

Social Security Normal Retirement Age

For many decades full retirement age was sixty-five. In recent years, the Social Security Normal Retirement Age was increased. The increase is being phased in so that, depending on the year you were born, normal retirement age is sixty-six with future retirees born in later years having to reach sixty-six and a half or sixty-seven for full retirement. The gradual increase in age has been put in place because people are living longer and the Social Security Administration needs to reduce its financial obligation.

If you don’t know your Social Security Normal Retirement Age, you can find out by calling the Social Security Administration at (800) 772-1213 or by looking it up on their website, www.socialsecurity.gov. If you become disabled more than twenty-nine months before your Normal Retirement Age, you will become eligible for Medicare before your full retirement age.

Tips for Counting Your Disability Benefit Waiting Period

Here are two tips for counting the unpaid disability waiting period. First, the month in which you become disabled does not count as one of the five unpaid months. The second tip is an exception to the first rule: If you become disabled on the first or second day of a calendar month, Social Security will count the month you became disabled as part of the unpaid waiting period.

Social Security Retirement after Disability

If you receive disability benefits after receiving reduced early Retirement benefits, when you reach your Social Security Normal Retirement Age there will be another change in your benefit amount. At that time, the Social Security Administration will switch you back to Social Security Retirement and your ongoing benefit typically will be less than your disability benefit, but more than your earlier reduced retirement benefit.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.