Medicare Savings Programs exist to help lower income individuals save money on care, prescription drugs, and even health insurance deductibles. They were developed as a savings program to help those Medicare beneficiaries with limited income see savings on commonly used health services. To understand the Medicare Savings Program in more depth, it’s helpful to know the four types and the details of income limits.

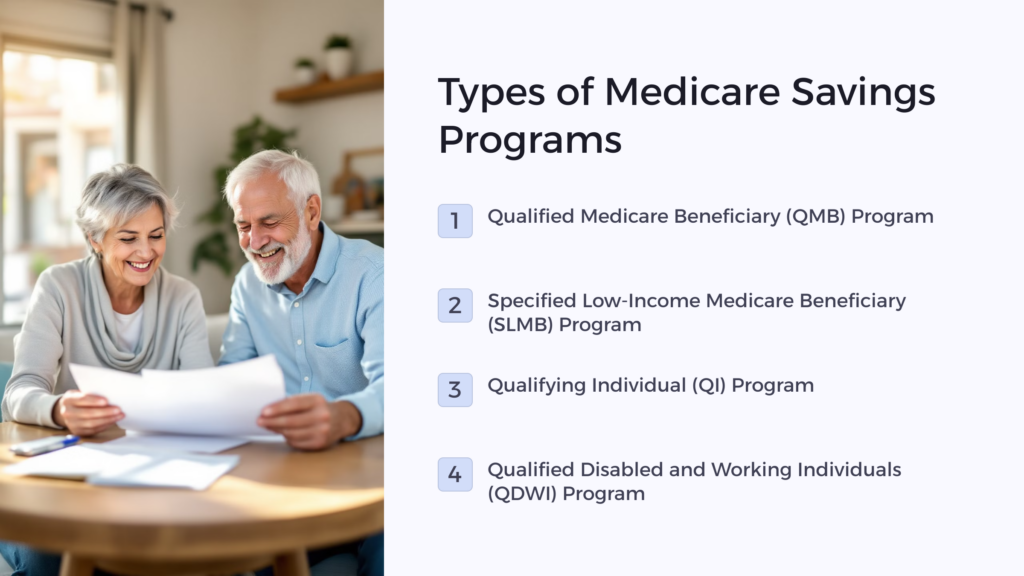

4 Types of Medicare Savings Programs

- Qualified Medicare Beneficiary (QMB) Program

- Specified Low-Income Medicare Beneficiary (SLMB) Program

- Qualifying Individual (QI) Program

- Qualified Disabled and Working Individuals (QDWI) Program

These four different savings programs can be tricky to tell apart because the devil is in the details—and those specifics relate to the monthly income a Medicare beneficiary and spouse earns, how many financial resources an individual or couple has, and whether or not the individual qualifies for other health insurance or low-income subsidies. It’s a lot to digest but the important point to focus on is that each of the four Medicare Savings Programs above has a somewhat different set of qualifications, which we explain below.

What is a Medicare Savings Program?

The Medicare Savings Program (MSP) is federally funded but run by individual states. The purpose is to help people who qualify for Medicare but are low income pay for health insurance premiums, deductibles, copayments, and coinsurance. To apply for the program, individuals can use either the Social Security Administration (SSA) online portal or call their state Medicare program. At the SSA website, there is a benefits eligibility screening tool that helps people make sense of which program applies to them.

After you become eligible for Medicare, you may be entitled to use one of these cost-sharing programs. In other words, the MSP shares the cost of Medicare with you. About three months after you officially become a Medicare beneficiary, the state will start paying the Medicare Part B premium and your Social Security check will increase a bit. Members will be reimbursed by the SSA (Social Security Administration) for each month of eligibility during which a Medicare premium was deducted from the beneficiary’s check.

To understand how the Medicare Savings Program works, it’s necessary to have a firm grasp on how the Medicare program works, or at least know the basics. Most people know that Medicare coverage is available to Americans aged 65 or older, and that there are different “parts” to the coverage. Medicare recipients do not get “free” health insurance coverage—they must pay for parts of the coverage. For low-income individuals, the Medicare cost can add up quickly. The MSP, then, is a type of low-income subsidy.

Medicare has four parts: A, B, C and D. Of these, Parts A and B are most relevant to qualifying (or not) for an MSP.

- Medicare Part A covers all inpatient or hospital coverage

- Medicare Part B is for outpatient and other (non-inpatient) medical coverage

- Medicare Part C gives beneficiaries an alternate way to receive Medicare benefits

- Medicare Part D covers prescription drug coverage

These different parts cover billing for specific services, which is why it’s important to understand them. Most Medicare beneficiaries decide to receive Parts A and B benefits through what is called “Original Medicare”, or the traditional fee-for-service option from the federal government. Original Medicare is also known as Traditional Medicare or Fee-for-Service (FFS) Medicare.

People like Original Medicare because it’s simple: The government pays directly for the health care services and recipients can go to any doctor, hospital, or clinic that accepts Medicare—and that’s 98% of medical facilities. With Original Medicare, there is often a need to purchase Medigap insurance to help pay for deductibles, co-payments, and co-insurance. Medigap is sold by private health insurance companies.

Private health insurance companies also offer more comprehensive Medicare plans, such as Medicare Advantage Plans, which usually cover prescription drug benefits. All you need to join such a plan is to know the date your Medicare number and the date your Part A and/or Part B coverage started.

What’s the Difference Between Medicare Savings and a Medicare Advantage Program?

A Medicare Advantage plan is simply a Medicare health plan offered by a private insurance company to contract with Medicare to offer all Medicare Part A and Medicare Part B benefits. You might also hear these plans referred to as “Medicare Part C” or “MA” plans. All private providers who participate must be Medicare-approved, and they must follow all rules Medicare sets forth.

Participating in a Medicare Advantage plan is another way to access your Medicare benefits. You’ll still have access to all your Medicare benefits, but you’ll be getting them through the Medicare Advantage plan, rather than through Original Medicare. You still retain all the same Medicare coverage associated with Original Medicare – they’re just administered through a private provider.

After you enroll in a Medicare Advantage plan, Medicare will pay that provider a fixed amount every month toward your coverage. In return, providers must follow all of Medicare’s rules about how those benefits are administered.

4 Types of Medicare Savings Programs

To figure out if you qualify for a Medicare Savings Program, you need to look at which parts (A, B, C, or D) of Medicare you pay for and/or want to pay for AND what your income and resources are to see if you qualify.

Qualified Medicare Beneficiary (QMB) Program

Perhaps the best known of the four MSPs is the Qualified Medicare Beneficiary Program, commonly referred to as QMB. How do you know if you are qualified? It is simple: You can qualify if you are receiving both Part A and Part B of Medicare and you meet the following income limits in 2020:

- Your individual monthly income limit is: $1,084

- As part of a married couple, your monthly income limit is: $1,457

Note: Income limits in two states—Alaska and Hawaii—are set somewhat higher. Also, if you earn income from a job, you could get the QMB benefits even if your income is higher than the limits listed above.

- Your individual resource (meaning all you own, which excludes your home) limit is: $7,860

- If you are part of a married couple, that resource limit goes up to $11,800

QMB will help pay for Part A premiums, Part B premiums as well as deductibles, copayments, and co-insurance.

Specified Low-Income Medicare Beneficiary (SLMB) Program

The SLMB helps pay Part B premiums for people who have Part A and limited income and resources. Remember, Part B is for any care not in a hospital (inpatient) setting but doesn’t include paying for prescription drugs.

- Your individual monthly income limit must be: $1,296

- If you are married, both spouses cannot exceed a monthly income limit of $1,744

As with the QMB program, these income limits are slightly higher in Hawaii and Alaska. If you have income earned from a job—then, like QMB, you could still qualify for benefits if your monthly income is higher than the limits listed above.

- The individual resource limit for this MSP is $7,860

- For a married couple, the total resource limit is $11,800

Qualifying Individual (QI) Program

This program tends to sometimes confuse people because it is very similar to the SLMB above. It also covers Part B premiums for people who have Part A. So, what’s the difference? With QI, the income limits are higher:

- Your individual monthly income limit must be: $1,456

- If you are married, both spouses cannot exceed a monthly income limit of $1,960

- The individual resource limit for this MSP is $7,860

- For a married couple, the total resource limit is $11,800

As with all the other programs we’ve described, limits are higher in Alaska and Hawaii. A Medicare beneficiary might choose QI if their monthly income is slightly higher, however, there is a catch. With QI, the SSA states on its website:

“You must apply every year for QI benefits. QI applications are granted on a first-come, first-served basis, with priority given to people who got QI benefits the previous year. You can’t get QI benefits if you qualify for Medicaid.”

There are restrictions and that can complicate your application—but if you make a little more income, the extra effort is worth the trouble.

Qualified Disabled and Working Individuals (QDWI) Program

The last of the Medicare Savings Programs is quite different from the other three. QDWI (Qualified Disabled and Working Individuals) is tailored to people who work but are also disabled. However, there is a bit more to it than that. As you will see below, the qualifications are quite specific and with QDWI you get help to pay for your Part A premium (inpatient or hospital coverage).

You might qualify if you fall into any of these categories:

- You are under 65, are working, and are disabled

- You went back to work, but lost your premium-free Part A insurance

- The state you reside in providing no other medical assistance or health insurance

- Like other plans, you don’t exceed the income and resource limits for your state

The limits for QDWI are as follows:

- Your individual monthly income limit must be: $4,339

- If you are married, both spouses cannot exceed a monthly income limit of $5,833

- The individual resource limit for this MSP is $4,000

- For a married couple, the total resource limit is $6,000

You’ve probably noticed that these income limits are much higher than for QMB, SLMB or QI Medicare Savings Plans. This is simply because SSA expects employed individuals (even if disabled) to earn more monthly income.

Do I Qualify for a Medicare Savings Program?

Without a little research, you won’t know if you qualify for QMB, SLMB, QI, or QDWI. However, if you meet the following basic requirements there is a good chance you will be able to take advantage of one of them:

Reside in one of the 50 states or the District of Columbia

This is self-explanatory but important to know if you are living across a border, such as in Canada or Mexico, or if you reside in Puerto Rico or other US-affiliated places that are not US states.

Are age 65 or older

The age limit is inflexible, but SSA recommends looking into your options at least six months before turning 65.

Receive Social Security Disability benefits

As a disabled person, you will probably qualify for some type of MSP and you should take full advantage of it.

People with certain disabilities or permanent kidney failure (even if under age 65)

Certain disabilities have special federal laws associated with them, and a full explanation for this can be found on the SSA web page that discusses what is unique about kidney failure. It boils down to the cost of long-term treatment (dialysis) which is the only known treatment for advanced kidney disease.

Meet standard income and resource requirements

Income and resource requirements are listed above but keep in mind they are not the last word. Sometimes, you can exceed the income limits and still qualify for a Medicare Savings Plan.

Medicare Savings Programs

Medicare is complicated to understand, no matter what your education level or income. The savings plans we’ve discussed are a form of cost-sharing that help people with fewer resources pay their Medicare costs. They provide people who need help with a Medicare supplement to offset the cost of all types of care and one of the most expensive aspects of health insurance: drug prescriptions.

It is important to know that the states administer the Medicare Savings Program, which means the income limits may vary. Your countable income is calculated in a very specific way, as is your asset limit. In all states, however, your house and car (and several other assets) will never be included in your asset or resource limit.

The bottom line when deciding if you qualify for a savings program is to start by looking at income and assets. Those numbers will help you understand what kind of help you can get through an MSP.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.