Learn about deemed income and resources and how they can affect an SSI application for children.

Deemed Income and Deemed Resources

Because Supplemental Security Income (SSI) is a needs-based assistance program, before a child’s SSI disability claim is reviewed medically to determine that disability exists, the claim is reviewed to see if the child meets the financial requirements for eligibility. This includes a review to see whether the child income or resources are to be deemed from his or her parents’ income and resources.

Deemed resources and deemed income refer to the portion of the SSI-ineligible parent’s or stepparent’s income and resources that are considered available for a disabled child’s support. Deemed income is used in calculating your child’s SSI payment and both income and resources are factored in when determining whether the child’s resources are below the SSI resource limit.

Generally deeming does not apply if the parent does not live with the disabled child. Exceptions include temporary absence, such as a child going away to school or an ineligible parent being absent due to a duty assignment as an active member of the armed forces.

Deeming Resources to a Disabled Child

If the applicant is a minor, unmarried child, and the child lives with a parent or stepparent (when the parent is in the household), a portion of the parent’s resources may be deemed too, that is counted toward, the child’s individual resource limit of $2,000. If the child has one parent living with him or her, then the parent can have $2,000 in countable resources before any of the parent’s resources are deemed. If the child has two parents—natural, adoptive, or stepparent—in the household, then the two parents can have $3,000 in countable resources before any resources are deemed to the child.

Many assets are not resources for SSI eligibility. Some examples of excluded resources are property used for self-support, often one vehicle, and a home in which the ineligible parent and disabled child live, and for a period of time, federal tax refunds.

Let’s look at an example.

Let’s say that a disabled child is living with her mother and stepfather. Her mother has assets of $500.00 in her name and her stepfather is buying the home they live in and has cash assets in his name of $3,500 for a total of $4,000 in countable resources for the two of them. The house is excluded. The eligible child has a small bank account with $75 in it. This means that the child has $1,075 in countable resources—her $75 bank account plus $1,000 deemed from her parents. Her total resources are below the $2,000 individual limit, so she qualifies for benefits as far as resources go.

It’s worth noting that deeming from a stepparent occurs only if the disabled child’s natural or adopted parent also lives in the household. Let’s continue the example we were looking at. In April 2018, the child’s mother moves out of the household and the child continues to live with her stepfather. Beginning the first of the following month, May 1, 2018, Angela is no longer subject to deemed resources. Only her own $75 account is considered a resource, even though her stepfather has more than the $2,000 in assets.

And, let’s look at the example one more time. If the family has two disabled children, then the $1,000 that is deemable would be divided in half with $500 deemed toward each child’s $2,000 limit.

Factors that Determine Deemed Income

The amount of income that is deemed to a disabled child from his or her parent or parents depends on the amount of countable income the parents and any ineligible children in the household have. It also depends on whether the parents’ income is earned or unearned, the number of ineligible children in the household, and whether an ineligible parent is sponsoring a non-citizen. Like resources, some kinds of income are excluded from deeming. In addition, part of the parents’ earning income is excluded under the earned income exclusions.

Calculating Deemed Income from Parent to Child

Several steps are involved in calculating the amount of income, if any, that is deemed to an SSI child applicant. First, part of the parents’ income is allotted to care for other children in the household who do not receive public income maintenance. The allotted amount is used to reduce the parents’ income in the deeming calculation. The amount of the allotment per child is equal to the difference between the unreduced Federal SSI Benefit Amount for a couple and the unreduced Federal Benefit Amount for an individual. In 2025, the difference between the $1,450 couple SSI benefit rate and the $967 individual rate is $483. This amount is reduced by certain types of income the child or sponsored alien may have. An allocation is also deducted for any SSI-eligible alien whom the ineligible parents’ sponsor.

The allocations for the children and sponsored alien are first used to reduce the ineligible parent’s unearned income. If the parent does not have enough unearned income to offset the allocations, the allocations will be applied to the parent’s earned income.

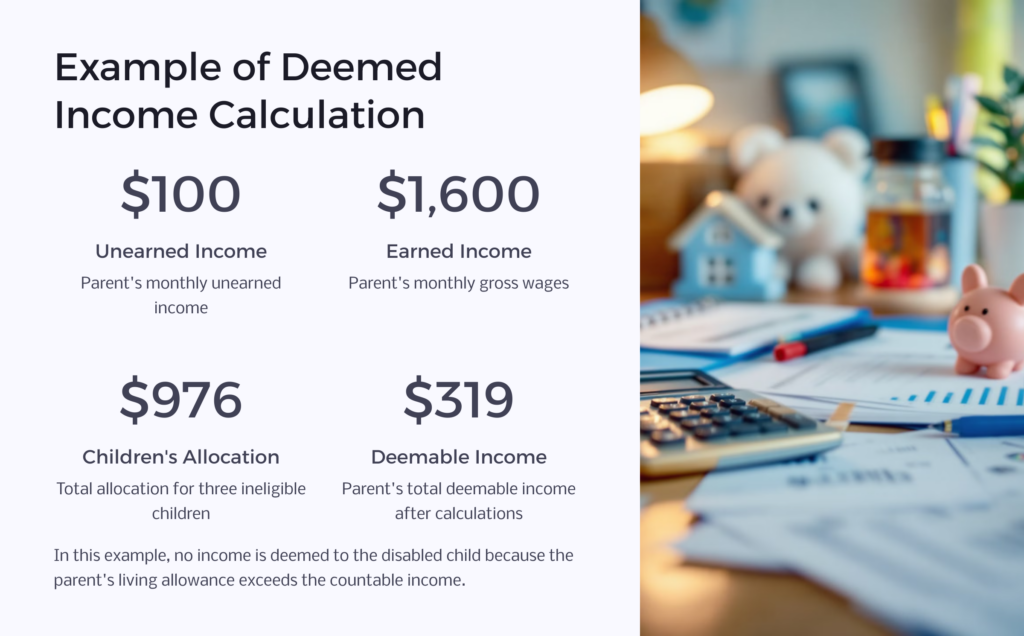

Example of Deemed Income Calculation

In a one-parent household, the ineligible parent has $100 unearned income and $1,600 a month gross wage. The family has three ineligible children, one of whom receives child support in the amount of $200 a month. Here’s how the Social Security Administration would figure out the amount of income to be deemed.

Calculation of Children’s Allocation

$392.00 Unreduced allocation for first child

– 200.00 Child support

$ 192.00 Allocation for first child

+392.00 Allocation for second child

+392.00 Allocation for third child

$976.00 Total children’s allocation

Calculation of Parent’s Deemable Income after Children’s Allocations

$100.00 Parent’s unearned income

– 100.00 Portion of children’s allocation

0 Parent’s remaining unearned income

$1,600.00 Parent’s earned income

– 876.00 Remaining children’s allocation

$ 724.00 Parent’s remaining earned income

Next, SSA applies the $20 general income exclusion and the earned income exclusions of $65 and one-half of the remainder to the parent’s remaining earned income.

$724.00 Remaining gross work earnings

– 85.00 $20 General exclusion and $65.00 earned income exclusion

$639.00

– 2 Second earned income exclusion

$319.50 Countable earned income

The countable earned and unearned incomes are combined.

$319.00 Parent’s countable earned income

+ 0 Parent’s remaining countable unearned income

$319.00 Parent’s total deemable income after children’s allocations and general and work exclusions

The last step is to subtract the ineligible parent’s living allowance, which is equal to the SSI federal benefit rate of $967.00 for an individual, from the countable parental income. Because the parent’s living allowance is more than the countable income, no money is deemed to the disabled child and the maximum SSI benefit of $967.00 is payable. (Note that if the child had two parents in the household, the couple allocation would have been $1,450.00.)

A Few Important Considerations

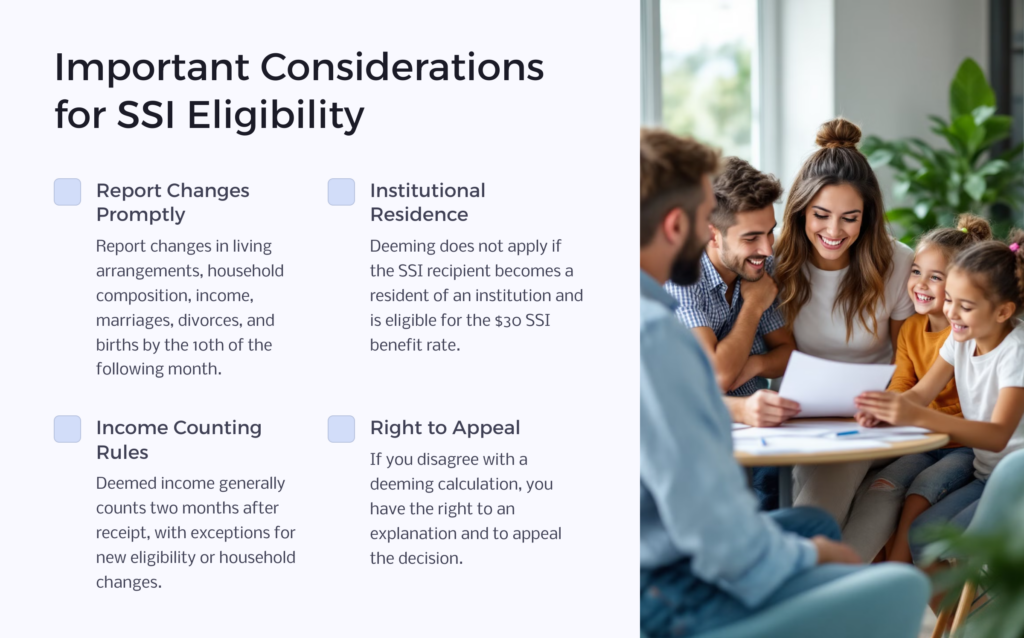

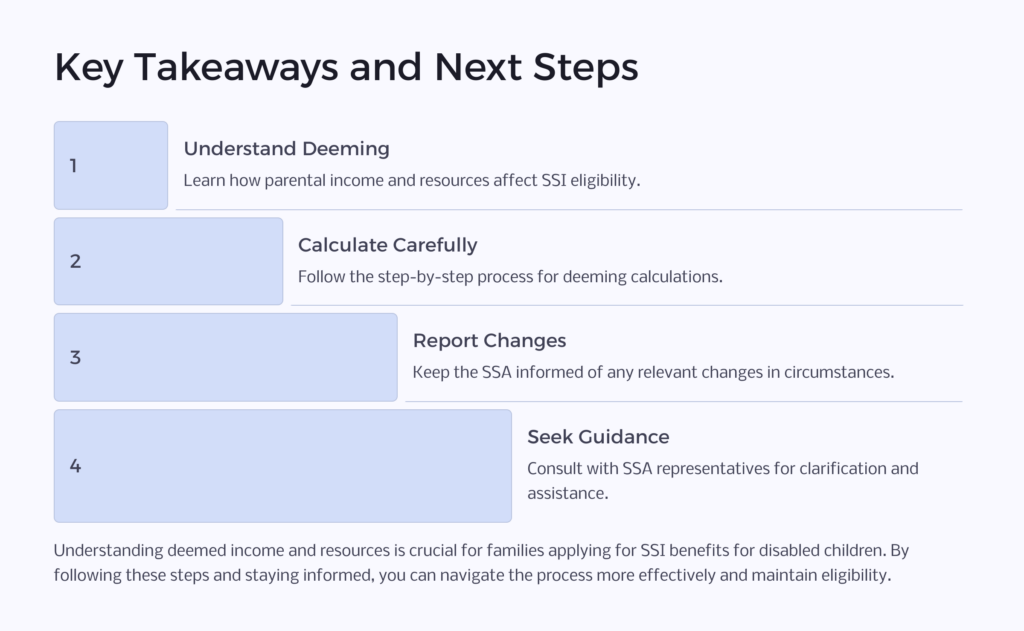

Be sure to report changes in living arrangement including admission to institutions, changes in household composition, that is, changes in who lives in the household. Also report changes in income, marriages, divorces, and births because all these changes can affect deemed income and the amount of SSI due.

Deeming does not apply if the SSI recipient becomes a resident of an institution and becomes eligible for the $30 SSI benefit rate.

Deemed income follows the general rule regarding when income counts, that is, two months following when it is received except when eligibility is just starting or restarting after a month of ineligibility or there has been a change in marital status or household composition that affects the deeming formula or a change in living arrangements such as coming out of an institution.

The explanations included in this article address the most common situations. The laws that govern SSI financial eligibility are very complex and detailed. If your child’s SSI application is denied for deemed income or you believe that too much of your income and assets are being counted against your child’s SSI benefits, you have the right to an explanation of the calculation and then if you still disagree, you have the right to appeal.

Maintaining SSDI Disability Eligibility for a Child

What responsibilities does a representative payee have to maintain SSI disability eligibility for a child? Learn when a representative payee must set up a Dedicated Account & set aside funds and what’s needed to maintain SSI disability eligibility for a child.

General SSI Reporting Responsibilities

If you are a representative pay for either an adult or a child, it is your responsibility to report changes. Reporting all changes by the tenth of the month following the month of the change will allow you and the Social Security Administration to stay current on the child’s SSI disability eligibility and financial eligibility.

In addition, you must open and manage a Dedicated Account if the disabled child for whom you are a representative payee receives a large past-due SSI payment and Social Security advises you that the money must be put in a Dedicated Account. The account must show the child as owner and that you manage the funds.

Past-due payments that require deposit in a Dedicated Account cannot be mingled with the child’s other resources and use of the funds is restricted to educational expenses, job skills training, and medical expenses. Social Security may also approve use of the funds for impairment-related needs such as in-home nursing care, special equipment, housing modifications, and therapy or rehabilitation. The money in the Dedicated Account cannot be used for basic monthly maintenance of food, shelter, or clothing, and other regular purchases. Because the money in the Dedicated Account cannot be used for food or shelter, it does not count toward the individual resource limit of $2,000.

The representative payee must keep bank records and receipts for at least two years to prove use of the funds and provide an explanation of how each expenditure relates to the child’s disability. If you stop being the representative payee, you must provide an accounting and turn the funds over to the new payee. If the disabled child turns eighteen and remains eligible for SSI as an adult, the restrictions on use of the dedicated funds remain in place. This is true even if the adult child is his or her own payee.

Don’t be overwhelmed by the rules of SSDI: At Benefits.com, we are here to help you navigate the process and receive the benefits you deserve. Begin today by taking our free eligibility quiz.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.