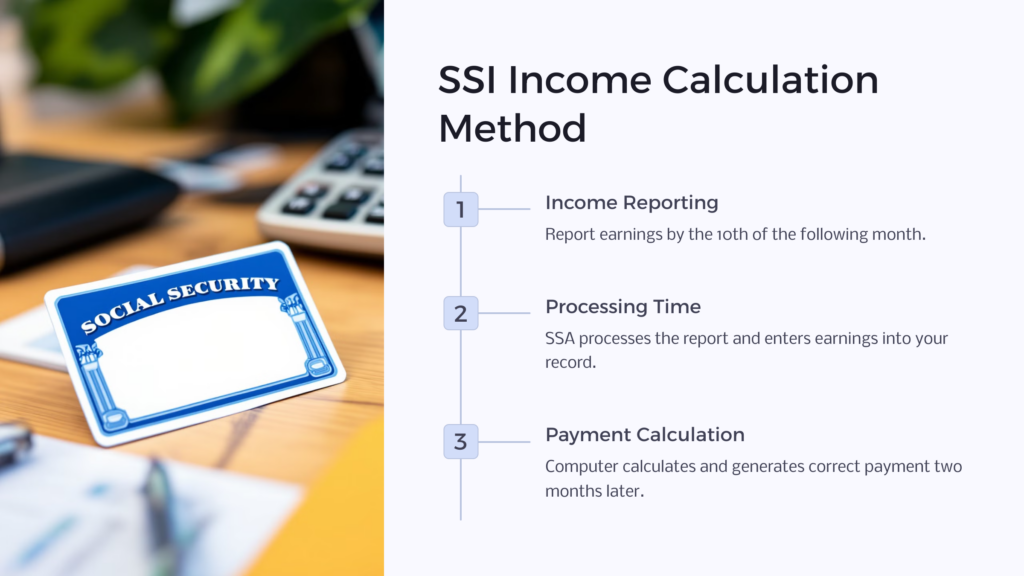

Supplemental Security Income (SSI) benefit amounts are based on income received in a month. When income is low enough to allow payment of SSI, income received in one month counts in determining your benefit two months later. This is called prospective accounting because it uses your income in one month to figure out your payment amount two months later. For example, income that you receive in March that is within the SSI income limits determines your SSI payment amount in May.

Understanding When SSI Counts Income

The reason for this accounting method is to reduce or eliminate overpayments (being paid more than you are due) and underpayments (being paid less than you are due). If you report your earnings and other income received in one month by the tenth of the following month, as is required, that gives the Social Security Administration (SSA) time to process your report and enter the earnings into your computer record for the computer to calculate, generate, and deliver a correct payment to you two months later.

There are two principal exceptions to this prospective accounting. The first is when you first become eligible for benefits. At that time, all your income in the first payment month counts in that month. Then during the next two months any recurring (ongoing) income received in the first payment month counts again in the second- and third-months’ benefit calculations. After that prospective accounting begins and the income you received in the second month counts in the fourth, and so on. For example, you apply in April and benefits start in May. May’s income counts in determining your benefits for May, June and July; then June’s income determines August’s benefit. Even this exception has an exception! If you had income the first month, May in this example, that was a one-time payment, that one-time income would count only in May.

The second primary exception occurs when you have been receiving benefits and have an increase in income that raises your countable income above the SSI limits. When that occurs, the income counts to determine your benefit for the month in which the excess income is received, and you would be ineligible in that month. Then in the following month, the calculation is the same as it was when you started to get SSI, that is, income received the first month after ineligibility counts for three months. Here’s an example: you have been getting benefits for the past eight months and then in March 2020, you receive extra income that puts your income over the SSI limit. You are not eligible in March and when your income drops within SSI limits in April, your April income determines your SSI benefit for April, May, and June before you return to having your income in one month count two months later.

How Overpayments Occur When Rate of Pay and Hours Remain the Same

So, this gets us to the question of how an overpayment can occur when a person is working the same amount and being paid the same rate of pay all along.

Here’s the underlying answer: people who are paid weekly or bi-weekly (every two weeks) are periodically paid an “extra” paycheck. Weekly-paid employees receive five instead of four paychecks every three months; bi-weekly-paid employees receive three instead of two paychecks every six months. This occurs because there is an extra payday (Friday, for example) in the month every three months for weekly employees or every six months for bi-weekly employees.

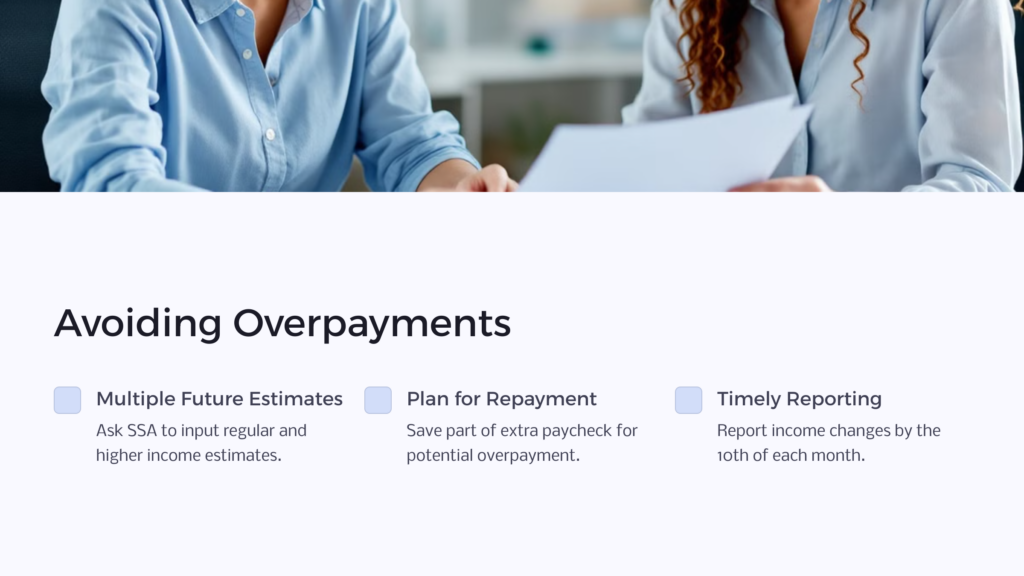

If the extra paycheck puts the disabled person’s income over the SSI limits, the disabled person can expect to be ineligible that month and be overpaid for the month. To avoid this situation, you can ask to have more than one future estimate put on the SSI computer record, that is, your regular income input for two (or five) months and the higher income input to the record at the same time for the third (or sixth) month.

If you are unable to arrange that or need the SSI payment on the first of the month for cash flow to cover expenses until the paychecks come in, expect that an overpayment will occur in the month of ineligibility. Usually, the overpayment will have to be repaid. Accordingly, it is advisable to use part of the extra paycheck to replay the overpayment promptly.

The reason you need to plan on repaying the overpayment is that after you are overpaid once due to increased income and the same thing occurs again, it is unlikely you will be granted a waiver of repayment because you would be at fault in keeping the SSI money you knew you were not eligible to receive.

If the extra paycheck does not cause ineligibility and is counted two months later, the SSI payment will be reduced in a month that you do not have an extra paycheck, so it would be a good idea to save part of the extra paycheck in one month to help pay expenses two months later when the SSI is reduced.

In summary, you should be able to avoid overpayments and underpayments as long as your income is within the SSI limits, and you report prior-month income changes on time by the tenth of the month and possibly by setting up advance estimates for months with known higher income. You can also strategize as described to minimize the impact of repaying overpayments and the impact of irregular SSI benefit amounts.

How Can Homeowners Getting Supplemental Security Income (SSI) or Social Security Disability (SSDI) Increase Their Income?

Learn how disabled homeowners can increase cash flow without debt and still keep their SSDI and SSI disability benefits.

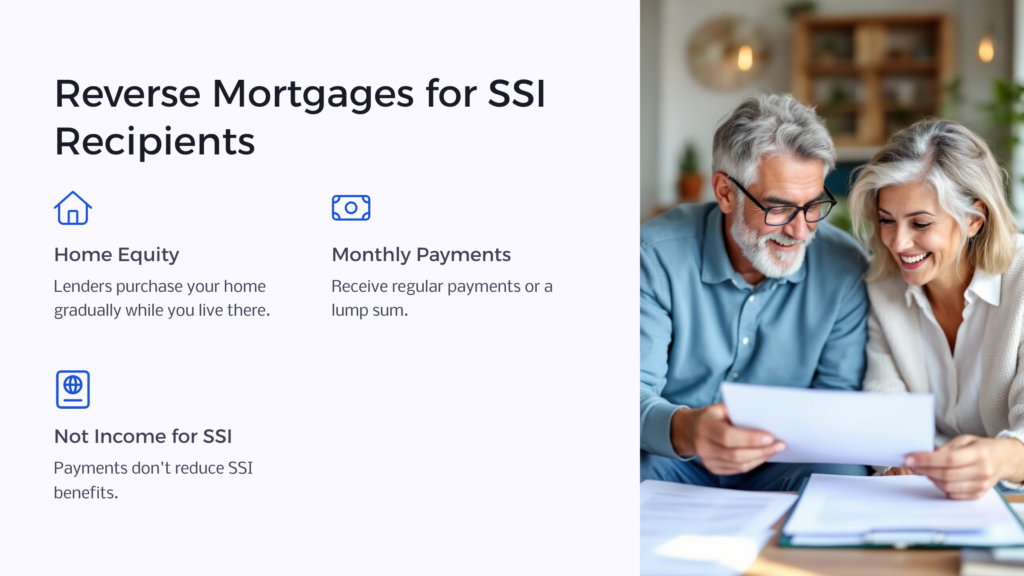

Whether receiving Social Security Disability (SSDI) or Supplemental Security Income (SSI), living on a fixed income can be difficult and the choices for a disabled person to increase income are limited. One option for homeowners who are at least sixty-two years of age if is a reverse mortgage.

What is a reverse mortgage?

If you own or are buying the home you live in and you and anyone who co-owns the property with you are at least 62 years of age and you have a large percentage of equity in your home, some lending institutions—banks, credit unions, and mortgage companies—will purchase your home from you little by little while you continue to live in it paying you a monthly payment. The way it works is that a bank, for example, will send you regular monthly payments while you retain full rights to live in your home or will give you a large lump sum while you retain the rights to live in the home. The amount of the payments depends on the value of the property, how long the reverse mortgage is set up for, and other factors you work out with the bank.

A reverse mortgage puts a lien on your property that must be paid, but not while you are living in your home. When you die or move out of your home, the property must be sold and the reverse mortgage payments plus interest paid back to the bank from the proceeds of the sale. (This is not a bank sale of your home; rather you or your heirs sell the home, and the bank lien is satisfied when the sale of the house is finalized, just like a regular mortgage.)

If you take monthly reverse mortgage payments, gradually, your equity in the property (portion of your property that you own) goes down, but you still get to live in your home while you have additional income to meet your current needs.

Reverse Mortgages and SSI

A reverse mortgage can be a great option for any disabled or retired person who is challenged in being able to take care of their current needs, but it is an especially good resource for individuals who receive Supplemental Security Income (SSI) because the reverse mortgage payments are not income and do not reduce SSI benefits.

Here’s the reason: With a reverse mortgage you are borrowing money and incurring a debt that must be repaid when you no longer live in the home. Because the money must be repaid, the money received is a bona fide (true) loan and is not considered income for SSI benefit calculation. Additionally, a debt is not a resource and the home you live in does not lose its excluded status when your resources are counted. (Do note, though, if you save the reverse mortgage payments and have the money on hand in the month after it is received, it does count toward the SSI resource limits in those subsequent months.)

Exercise Caution

Of course, a reverse mortgage is not for everyone, but if you think it might be for you, Disability Advisor suggests that you shop around with various financial institutions to see what might work best for you and, of course, that you fully understand all papers you sign before entering into any agreement. To be certain you make the best choice for yourself, consult with a real estate attorney and/or a financial advisor to be sure that a reverse mortgage is the right choice for you.

In short, a reverse mortgage does not automatically disqualify a homeowner for SSI, but the homeowner must be careful with the timing of spending of the reverse mortgage funds. You should contact your SSI administrator to determine exactly how to comply with the SSI eligibility requirements if you take out a reverse mortgage.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.