Veterans are able to purchase a home with the help of a VA Loan. These loans typically provide favorable rates, an easier qualification process, and no down payment. Even so, sometimes a veteran – just like anyone else experiencing financial hardship – might face foreclosure proceedings.

7 Ways For Veterans To Avoid Foreclosure

- Loan Modification

- Repayment Plan

- Special Forbearance

- Deed-in-Lieu of Foreclosure

- Additional Time To Arrange Private Sale

- Short Sale

- Financial Planning

Contrary to what you might think, not all VA loans are provided and serviced by the Department of Veterans Affairs (in fact, most are not). Though the VA can serve as the lender with a VA direct loan, a veteran can also get a VA-backed loan from a private lender or mortgagor.

Since the VA is backing a portion of the loan, the lender may offer more flexibility around VA loan eligibility. Around 90% of such VA-backed loans are offered without the requirement for a down payment. Some things about the VA loan are similar to a conventional mortgage. For example, although there are no closing costs, there is still a VA funding fee.

What Is a VA Loan Foreclosure?

When a homeowner can no longer make their monthly payments or repay the loan, their home will go into foreclosure. This process involves the lender exercising their lien on the property and taking it as collateral to cover their losses from the defaulted loan.

The rules have changed a little bit over time regarding VA loan foreclosures. If the loan closed before January 1, 1990, the borrower will have to pay the government back for covering the loan and paying off the lender. If the loan closed after that date, the defaulted borrower only has to pay it back if evidence of misrepresentation, bad faith, or fraud was found.

7 Ways For Veterans To Avoid Foreclosure

It’s important to note that the VA cannot help you if the foreclosure process involves a home purchased with one of several different types of FHA loans. However, the following tips are still generally applicable no matter what type of loan you have.

1. Loan Modification

A loan modification allows you to temporarily let go of missed payments, adding them to your owed balance, along with any legal fees associated with the foreclosure. You can then work out a new loan or new loan terms with your lender based on the outstanding balance.

While a VA guaranteed mortgage is backed by the VA, they typically only back 25% of the loan – or around $36,000. This means that the lender stands to lose a significant amount if the home goes into foreclosure.

Banks and lenders do not want to lose their money and gain your property. In most cases, they sell off a foreclosed home at a loss. It’s in their best interest to rework the terms of the loan so they can continue to collect their money, so don’t be afraid about approaching them with this idea.

2. Repayment Plan

A repayment plan is a good solution when a few payments have been missed, but the borrower has the potential to repay the loan. The homeowner just needs the VA loan repayment to be restructured so they can catch up and continue making their monthly payment. This restructuring usually just involves continuing to make the monthly payment plus an appended amount to recapture the missed payments.

3. Special Forbearance

Special forbearance facilitates making up payments you have missed by giving you more time to make them. This might be a good option if your inability to make payments is due to a short term financial hiccup, such as a serious car repair that drained your rainy day fund or the temporary loss of a job. If the downturn in your finances is going to be for a longer term, then special forbearance will not be an adequate bandaid.

4. Deed-in-Lieu of Foreclosure

A deed in lieu of foreclosure means signing over the home to your lending servicer to avoid foreclosure proceedings. Though you will lose the home, the outstanding debt will be forgiven so that the bankruptcy does not blemish your credit report (note that your credit will still be impacted).

One situation where this particular choice among loss mitigation options might be concerning is when a surviving spouse of a veteran cannot maintain the property and the mortgage. They can walk from the home, downsize their housing obligations, and maintain their credit score so that their future financial options (such as leasing a vehicle) will not be impacted by a sudden life event.

Most lenders do have specific requirements that must be met before seeking this option, such as attempting to sell the home for at least 90 days, providing pay stubs, and submitting a hardship letter.

5. Additional Time To Arrange Private Sale

Some lenders may be willing to give you time to find a private buyer for the home. The home buying process does take time, so this option may not be best in every situation. If the value of the home is below what the borrower owes (meaning, the home is said to be underwater), this won’t entirely solve the problem.

However, in these cases, there is our final listed option, the short sale. Larger institutional lenders may not extend this type of option, but a smaller loan servicer might. If you got your VA loan from a private lender who sells repackaged home loans, this might be a good way to avoid a VA loan foreclosure.

6. Short Sale

If your home is underwater, this means that the market value of the home is less than what you owe on the property. The lender might agree to a short sale, which means they’ll take whatever they can get from the sale and forgive the loan. While larger lenders may not give you additional time to arrange a private sale, they may be willing to settle for a short sale. Unlike a deed-in-lieu, a short sale may impact your credit score a little bit more.

7. Financial Planning

The best defense is a good offense, as they say – something a service member might be well familiar with having served in the military. The most common reasons a borrower defaults on their home loan are debt and emergencies – both of which (believe it or not) can be alleviated with preparation.

Debt can be avoided by spending within your means, something that can be achieved with budgeting and commitment. For example, many mortgage lenders will not extend a mortgage loan to a borrower unless the monthly mortgage payment will be 28% or less of their income.

They also consider debt service, which is the amount of money the borrower must take to pay off their debts – not just their mortgage but also other debts like credit card debt, student loans, and car loans. Anything above 36% is viewed as a credit risk.

These numbers should serve as a good guide for any potential borrower, whether they are seeking a conventional loan or a VA mortgage. Of course, there are also life surprises such as the loss of a job or a medical emergency. Allocating a portion of your income into a savings account or a rainy day fund is a great way to avoid a missed payment and risk losing your VA mortgage loan.

Of course, sometimes even budgeting and advanced planning cannot stop an emergency from sending your home towards the status of a foreclosed property. In these instances, you can proactively reach out to your mortgage servicer and the VA to discuss options and resources.

If you know ahead of time that you are going to probably miss a payment on your mortgage, you should be proactive and notify your VA lender or loan officer. In the end, this ab initio treatment will probably result in a lot less damage than looking back ex post facto.

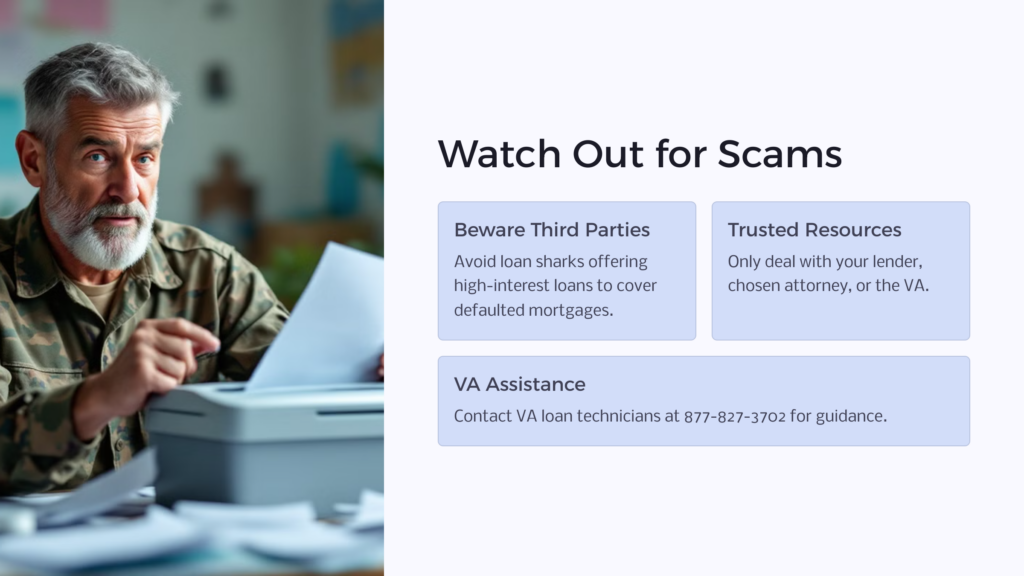

Watch Out for Loan Relief Scams

You must be vigilant against third parties who offer assistance in dealing with your loan. These loan sharks might offer high interest swing loans to cover your defaulted mortgage and trap you once again in unpayable debt.

As a general rule, you should only deal with your lender, an attorney you have chosen to work with, or the VA. Certified VA loan technicians are available at 877-827-3702 and will speak with you even if your loan is VA guaranteed loan and not VA direct. If you are a VA borrower and are not sure how to approach your lender, the VA can provide you with guidance.

What About the SCRA?

The Servicemembers Civil Relief Act can help active duty service members whose conventional loan obligation began before active duty service. In some cases, the SCRA can help a service member whose loan obligation began after active duty.

The SRCA can only stop a foreclosure sale for properties purchased before active duty service. Therefore, they are not relevant for a VA foreclosure. At the same time, is important to note the benefits of the SRCA, because it can prevent evictions (as long as the rent is below $4,089 per month, a threshold that is unlikely to be crossed for most rentals), repossession of a vehicle, liquidation of items at a storage center, or being subpoenaed for a civil proceeding like divorce or child support.

The SCRA was meant to protect service members from financial loss at times when they cannot defend themselves in a civil suit because they are actively defending the country. However, it is usually not a useful tool for a VA borrower to prevent a VA foreclosure.

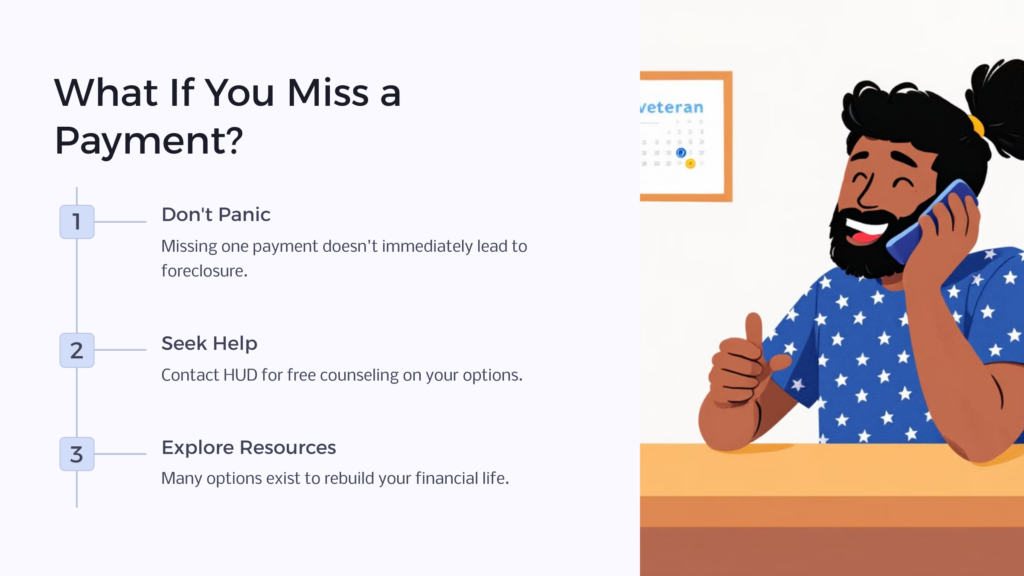

What Happens If I Miss a Mortgage Payment?

Don’t panic if you miss a monthly payment on your VA loan. The Department of Housing and Urban Development (also known as HUD for short) offers free counseling and can help you go over your options. HUD is dedicated to keeping veterans in their homes and helping homeless veterans find suitable housing.

It’s common for someone experiencing financial hardship to feel hopeless. However, there are plenty of resources out there to help rebuild your financial life and get back on track. This is especially true for veterans who have earned benefits in repayment for the service and sacrifice they have made for their country.

Avoiding VA Loan Foreclosure

Foreclosure can happen to anyone. And even though VA loans are among the many veterans benefits that can help service members transition to civilian life, a veteran can still fall into financial hardship and default on their loan.

Thankfully, several options are available to help prevent foreclosure or mitigate its consequences. If you need help with your VA mortgage, speak to the VA, your attorney, or your lender about choosing the best financial strategy for avoiding foreclosure.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.