If you’re ready to buy your dream home or you’d like to refinance your current home, you probably know that one of the most helpful veterans’ benefits is a VA mortgage loan. With this type of VA loan, there’s no down payment and no private mortgage insurance. But what if you have bad credit?/

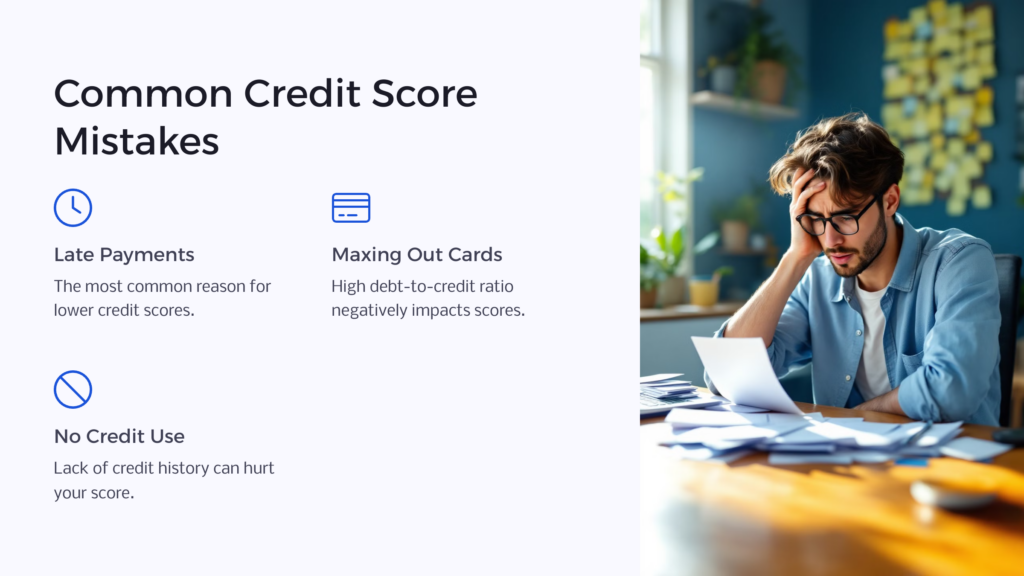

6 Mistakes That Hurt Your Credit Score

- Making late payments

- Maxing out credit cards

- Not using credit at all

- Filing for bankruptcy

- Not checking your credit report for mistakes

- Closing accounts in good standing

You may have doubts about your credit score and wonder how healthy it needs to be in order to qualify you for your VA mortgage. Whatever your score is, don’t lose heart – it’s a snapshot of a moment in time, nothing more. There’s a lot that goes into determining your overall credit score and whether you obtain your Certificate of Eligibility – we’ll walk you through some of the most common mistakes that lead to lower credit scores, along with the outlook for being approved for a VA mortgage loan with a lower credit score. Keep reading.

Knowing your credit score is a great first step toward qualifying for any type of mortgage. If you’ve been turned down for a conventional loan in the past or have reason to believe your credit score is less than stellar, the first thing to do is take stock of the situation. Once you have your credit report in-hand, look through it carefully for mistakes that can pull your score down. Once you know what’s making your score lower than you’d like, you can take appropriate steps to get your score up and make you a more attractive candidate to a lender for any type of credit, including a VA mortgage loan.

Can I Get a VA Home Loan With Bad Credit?

The short answer is that it’s possible, but there are many different factors to consider. The first step is to define what you mean when you say, “bad credit.” Credit scores exist on a continuum, so while very few credit scores are perfect, there’s a wide range of what people might mean by “bad credit.”

In general, the VA loan program doesn’t have a specific credit score requirement or a minimum credit score it’s looking for – it specifies simply that any VA borrower must be a satisfactory lending risk, so that means that a VA loan specialist will look at a lot of different factors when reviewing your loan application, not just your credit score.

However, at the end of the day, the VA isn’t the entity actually loaning you the money for your mortgage. VA loans are guaranteed by the U.S. Department of Veterans Affairs, and while the VA loan program may insure a portion of your loan, the VA-approved mortgage lender is putting up the funds. They will still be on the hook if you default on your loan. That said, the VA loan program recognizes that active duty and retired military personnel may face financial challenges that civilian borrowers don’t, so it’s prepared to offer loans for lower credit scores.

In the current economic climate, a minimum credit score of around 660 is generally a VA loan

requirement for approving a mortgage loan. You can certainly have a few blemishes on your credit report and still score in the 660s. In some cases, you may have even survived a bankruptcy or foreclosure and still be able to hit this minimum credit score. On average, VA borrowers weigh in with credit scores a bit lower than most borrowers for a conventional loan – 709 compared with 730-750, respectively.

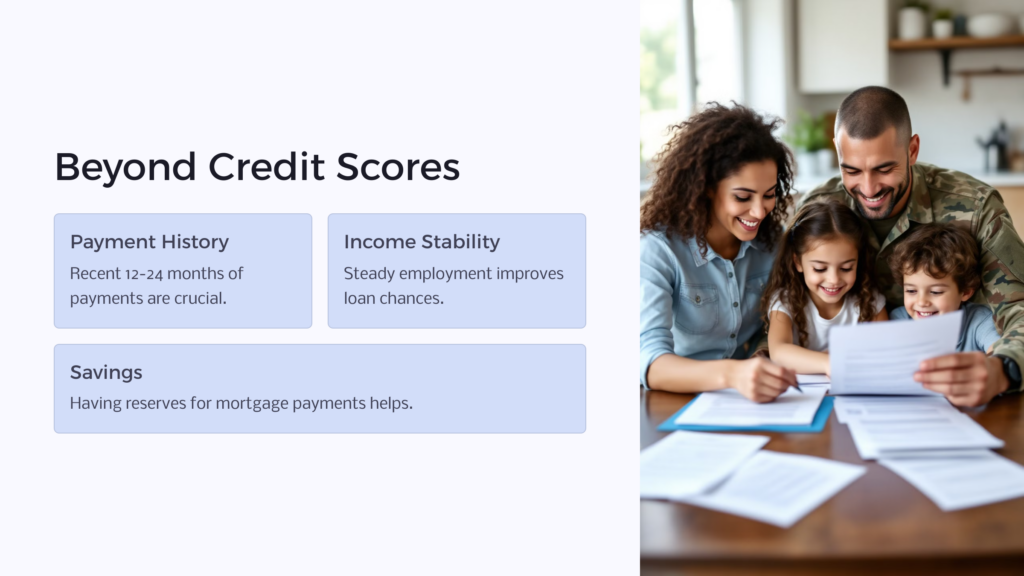

In addition to your credit score, the lender for a VA mortgage loan will consider several other factors – including your rent and mortgage payment history, your most current 12 months of payment history, and your most current two years of monthly payment history after a bankruptcy or foreclosure. If you have a healthy income, solid employment history, and enough savings to pay a few months of your new mortgage payment, you’re likely in good shape for loan approval.

6 Mistakes That Hurt Your Credit Score

There are several key factors that credit reporting agencies consider when calculating your credit score. Here are a few key mistakes that can make your credit take a nosedive:

1. Making Late Payments

Late payments are the most common reason someone may have a lower credit score. About 35% of your credit score is determined by your payment history – so every late monthly payment you make can bring your score down. If you have a history of late payments, that could be a very powerful influence on your total score, and if you’ve ever had an account go to collections, that information can stay on your credit report for up to seven years.

To help increase your score, make sure to start paying your bills on time if you’re not already, and if you are, make sure to keep on-time payments a top priority. The longer your history of on-time payments, the higher your score will be. If you have trouble juggling all your various due dates, try setting up automatic payments to make sure you never miss a deadline.

2. Maxing Out Credit Cards

The amount of overall debt you carry is another key component of your credit score. Ideally, you want to show that you are only using a small portion of your credit limit. When you run credit cards all the way up to the limit, that results in a high debt-to-credit ratio, which can lead to a lower score.

As a general rule, try to keep your overall credit usage under 30% for the highest credit score. If you’re over that amount and you can afford it, try to make a payment on your credit cards twice a month rather than just once. This can help lower your credit utilization, while also lowering the amount of interest charged per month. If you carry a balance on several cards, try to pay down the ones closest to their limits, which helps lower your overall credit utilization rate.

While some parts of the credit score algorithm are really hard to influence, paying your bills on time and keeping your debt-to-credit ratio as low as possible are two huge steps you can take to improve your lower credit score.

3. Not Using Credit at All

The flip side of using too much available credit is not using any credit at all. While it might seem smart to use a debit card or cash for all of your transactions, not using any credit at all means that there’s no record of how you use that credit. In order to be approved for a home mortgage, you’re going to need some kind of credit history, and preferably a positive credit history.

Fortunately, this is a simple issue to fix. You can simply apply for a small loan amount– maybe $500-1000 – and then pay it back quickly. You can also apply for a gas station credit card or a department store card; these are usually easy to get and have low credit limits. Just make sure that as you use your new cards, you pay your balance in full every month to keep building a positive credit history.

4. Filing for Bankruptcy

While bankruptcy can have some benefits for other reasons, depending on your financial situation, it’s generally a bad move when it comes solely to your credit score. In fact, it’s probably one of the very worst things you can do. A bankruptcy filing will certainly cause a score to plummet. Many mortgage brokers and car loan financing companies will automatically reject a credit report with a bankruptcy on it. If you are in a situation where it seems bankruptcy is your best option, you’ll need to slowly rebuild your credit. There’s no quick fix.

5. Not Checking Your Credit Report for Mistakes

Unfortunately, many credit reports will contain a mistake at some point. One government report has shown that up to 26% of consumers have a material error on their credit report that makes them look like a bigger risk in error. You don’t want to discover a mistake right when you’re in the middle of being approved for something as important as a home mortgage.

Make sure to regularly check your credit report for accuracy. Keep an eye out for accounts that aren’t yours, inaccurate information about payment history or amounts owed, inaccurate name or address information, erroneous Social Security number, or negative information older than seven years. If you do discover a mistake, the Federal Trade Commission has a clear procedure for getting them corrected. Under the Fair Credit Reporting Act, your creditors are obligated to correct any mistakes.

Once you’ve made improving your lower credit score a priority, regularly checking your credit report will let you know what kind of progress you’re making toward that goal. Seeing your progress regularly is inspiring and can help fuel even more success. Keep in mind that you’re guaranteed one free credit report per year from each of the three reporting agencies – Experian, Equifax, and TransUnion. Requesting one does nothing to damage your credit score. If you find a mistake, you can request a change, and this usually provides a pretty quick fix – your score can go up quickly once mistakes are changed. About 20% of people who request corrections to their credit reports see their score increase quickly, usually in between 10-30 days.

6. Closing Accounts in Good Standing

Maybe you have some credit cards that you never use. You might think that closing those accounts and removing them from your credit report is a good move. But this can actually hurt you.

Since your overall debt-to-credit ratio is a big part of your credit score, those accounts are helping you. Having that account open, with no credit used, increases the overall amount of credit at your disposal, which leads to a lower debt-to-income ratio. But when you close that account, that amount of credit disappears from your available credit, which drives up your debt-to-credit ratio and lowers your overall score. Better to keep the account open, while continuing to avoid using it.

Also, the age of your accounts can help boost your score. The longer you have an account open without maxing it out, the better that reflects on your score. It doesn’t matter that you’re not using that particular card. The fact that you’ve had a relationship with a creditor for a very long time works in your favor and helps boost your score.

VA Home Loans and Bad Credit

While it is possible to secure a VA home loan with less than stellar credit, that doesn’t mean you shouldn’t take the necessary steps to improve your credit score. The higher your credit score, the better the mortgage rate you’re likely to get, which will save you money over the long term. If you’ll review some of the major pitfalls and mistakes presented here, you can be confident in presenting the strongest credit score that can get you the best VA mortgage loan at the best rate for your new home.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.