The ability to access a home mortgage loan through the U.S. Department of Veterans Affairs is a tremendous benefit for eligible American military veterans. VA mortgage loans are available for veteran homebuyers with no down payment required. VA loans are typically easier to qualify for than conventional mortgage loans.

Using a VA home mortgage loan to purchase a home may translate to lower closing costs for the qualified veteran homebuyer. However, the VA does require a veteran home buyer to pay a funding fee, which can either be financed as part of the overall loan amount or paid separately at the time of closing.

How Is the VA Funding Fee Determined?

- Purpose of Loan

- Loan Amount

- Type of Loan

- Whether It Is a First-Time Loan or Subsequent Loan

- Down Payment Amount

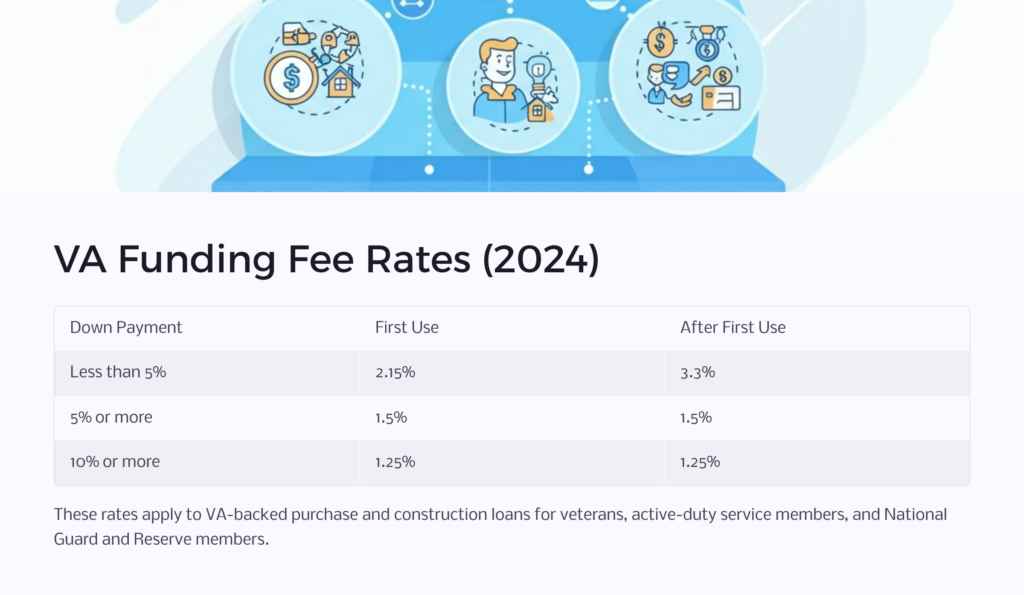

2024 VA Funding Fee Rates

VA-Backed Purchase and Construction Loans

Rates for Veterans, Active-duty service members, and National Guard and Reserve members

| If your down payment is… | Your VA Funding Fee is… | |

|---|---|---|

| First use | Less than 5% | 2.15% |

| 5% or more | 1.5% | |

| 10% or more | 1.25% | |

| After first use | Less than 5% | 3.3% |

| 5% or more | 1.5% | |

| 10% or more | 1.25% |

VA-Backed Cash-Out Refinancing Loans

Rates for Veterans, active-duty service members, and National Guard and Reserve members

| First use | 2.15% |

| After first use | 3.3% |

Native American Direct Loan (NADL)

| Type of Use | VA Funding Fee |

|---|---|

| Purchase | 1.25% |

| Refinance | 0.5% |

Other VA Home Loan Types

| Loan Type | VA Funding Fee |

|---|---|

| Interest Rate Reduction Refinancing Loans (IRRRLs) | 0.5% |

| Manufactured home loans (not permanently affixed) | 1% |

| Loan assumptions | 0.5% |

| Vendee loan, for purchasing VA-acquired property | 2.25% |

What Is a VA Funding Fee?

The VA funding fee associated with your VA mortgage loan is a one-time payment required when the loan is funded. Qualified veterans must pay this fee to offset the costs of VA mortgage loans for US taxpayers since these loans are backed by the US government.

By paying the VA funding fee, veterans help keep the VA home mortgage program operating well into the future. The program remains partly funded by U.S. taxpayers and partly funded by participants in the program. While the amount of the funding fee is determined by several different factors, it generally ranges anywhere from 0.5% to 3.3%.

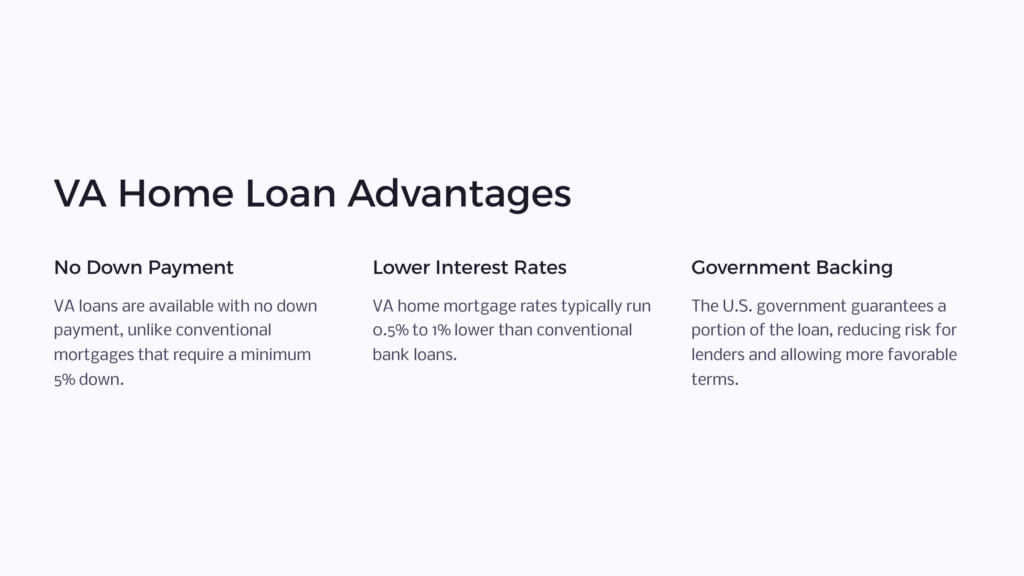

VA home mortgage loans have several advantages over conventional bank loans. For example, while a conventional mortgage requires a 5% minimum down payment, with 20% required to avoid mortgage insurance, VA home loans are available with absolutely no down payment. In addition, VA home mortgage rates typically run anywhere from 0.5 to 1% lower than conventional bank loans.

With a VA mortgage, the U.S. government is standing behind a portion of the loan granted by a private lender. In these cases, if a VA-backed home loan goes into foreclosure, this guarantee allows the lender to recover some, or in many cases, all of the financial loss. Since there is less risk, the lender can grant the loan under more favorable terms.

As a participant in the VA mortgage loan program, each homebuyer who enters into a VA home mortgage must pay a VA funding fee. The amount of the fee varies depending on the specifics of the loan circumstances and helps make sure VA home mortgage loans are available for veterans well into the future. It’s helpful to consider the VA funding fee as the VA loan equivalent of the private mortgage insurance typically associated with a conventional loan.

Who Is Excluded From Paying a VA Funding Fee?

All veterans using a VA mortgage to finance a home must pay the VA funding fee, with a few specific exceptions. For example, if the veteran receives VA disability benefits for a service-connected disability, this veteran will not be charged a VA funding fee. Sometimes, veterans who qualify for VA disability benefits after they receive their loan can have their funding fee refunded.

The VA also provides some exceptions for surviving spouses. For example, if the homebuyer is the surviving spouse of a veteran who died either during their time of service or from a service-connected disability, the surviving spouse may be exempt from paying the VA funding fee. The same is true of the surviving spouse of a veteran who was totally disabled as long as the surviving spouse also receives Dependency and Indemnity Compensation.

In addition, some active duty military members can avoid the VA funding fee. The homebuyer is exempt from the funding fee if they are an active duty military member with a disability rating for a pre-discharge claim. Active duty service members who have received the Purple Heart are also exempt from paying a funding fee.

The VA reserves the right to consider individual fee waiver requests on a case-by-case basis, and may at times offer exemptions that are outside of their guidelines.

Certificate of Eligibility (COE)

As a veteran seeking a VA mortgage loan, you’ll need to present a Certificate of Eligibility from the VA. This certificate guarantees to your lender that you meet the VA’s criteria for VA home loan eligibility. Eligibility requirements include completing at least 181 days of service during peacetime or 90 days of service during a time of conflict—or, completing at least six years of service in the Reserves or National Guard.

The surviving spouse of a military member who died in the line of duty or from complications related to a service-connected disability is also eligible for a Certificate of Eligibility from the VA. While this certificate is not needed to start the VA mortgage qualification process, it must be submitted to your lender before the process is complete.

How Is the VA Funding Fee Determined?

VA funding fees are determined on a case-by-case basis. The fee is determined by several different elements of the requested home loan:

Purpose of Loan

You may pay a different funding fee depending on whether you’re using your mortgage loan for a home purchase or construction, versus using your loan for a cash-out refinancing loan. For example, when you are using your VA mortgage loan to buy a home, your funding fee amount will vary depending on the amount of your down payment. For a first-time borrower, the funding fee for a home purchase can range from 1.25%, which is associated with a down payment of 10% or more of the purchase price, and 2.15%, with no down payment at all.

With a cash-out refinancing loan from the VA, the borrower’s funding fee is a flat rate of 2.15% for first-time use and 3.3% for all subsequent uses.

Loan Amount

Your VA funding fee is also calculated based on the total loan amount. So, the larger your loan, the larger your funding fee will be. This is based only on the loan amount—not the home’s total price. So if you’re buying a $300,000 home, but putting down a $10,000 down payment, your funding fee would be based on the $290,000 loan amount.

It’s helpful to put down as large a down payment as possible. Not only can it reduce your funding fee percentage, but reducing the amount of your loan also lowers the funding fee.

Type of Loan

There are several different types of VA loans, all of which affect the VA funding fee. You can get a VA mortgage for a home purchase or construction, plus cash-out refinancing. The VA also makes funding available for a Native American Direct Loan (NADL), Interest Rate Reduction Refinancing Loan (IRRRL), manufactured home loan, loan assumption, and vendee loan to purchase VA-acquired property.

Each of these loan types brings with it a different VA funding fee. For example, the funding fee for an NADL, intended to support Native American veterans as they purchase or build homes on federal trust land, is 1.25% for home purchase and 0.5% for a refinance, while the funding fee for a vendee loan is a flat 2.25%.

Regarding refinancing loans, the VA makes two options available: the IRRRL loan and a cash-out refinance. Funding fees differ slightly for these two programs, largely based on their foundational purpose. While the IRRRL loan is designed to help veterans lower their existing interest rates or to convert from an adjustable- to a fixed-rate mortgage, the cash-out refinance option allows veterans to take out cash from their home equity.

The funding fee for the IRRRL option is 0.5%, no matter the veteran’s service history or how many times the veteran has accessed a VA loan. With the cash-out refinance option, on the other hand, the funding fee starts at 2.15% with the first instance and rises to 3.3% for every subsequent use.

Whether It’s a First-Time or a Subsequent Loan

When determining your funding fee, the VA will consider whether you’ve ever used a VA home mortgage loan before. For first-time borrowers, the funding fee is 2.15% with no down payment. The rate increases to 3.3% with no down payment for borrowers who have previously purchased a home with a VA loan.

You’ll notice in the charts presented here, the funding fee evens out for first-time and subsequent borrowers as a down payment is made. For both groups of borrowers, the funding fee is 1.5% for a down payment of 5%, and 1.25% for a down payment of 10% or greater. So, if you’re using a VA home mortgage for at least the second time, you may want to put down at least a 5% down payment in order to reduce your funding fee.

Down Payment Amount

The amount of your down payment affects your VA funding fee since it helps determine the percentage of your loan amount. For example, VA loans with no down payment can come with a VA funding fee of 2.15 to 3.3%, depending on whether it’s the homebuyer’s first time applying for a VA loan. But by putting down a 5% down payment, the qualified veteran can reduce the VA funding fee to 1.5% – and to 1.25% by putting down a 10% down payment or more.

The amount of the down payment also reduces the total amount of money borrowed. A larger down payment results in a lower funding fee percentage calculated against a smaller loan amount, saving money over the life of the loan.

VA Funding Fees

VA home mortgage loans are a tremendous benefit the VA offers to qualified American veterans. If you’re thinking of purchasing a home or refinancing a mortgage, it’s worth checking whether you qualify and how a VA mortgage can save you money over the life of your home loan.

Once you understand how the VA funding fee is calculated, you can make an informed decision about the financial commitment associated with your home, including the funding fee and any other associated closing costs.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.