The Department of Veterans Affairs provides several life insurance options for veterans and active duty U.S. military service members, with the goal of increasing veterans’ peace of mind as they know family members are financially protected. The wide variety of options might feel overwhelming, but we’ve outlined everything here that you need to know to determine which kind of life insurance policy is right for you and your family.

6 Types of VA Life Insurance

The VA offers several different life insurance options, which we’ve outlined for you below.

- Servicemembers’ Group Life Insurance (SGLI)

- Family Servicemembers’ Group Life Insurance (FSGLI)

- Traumatic Injury Protection (TSGLI)

- Veterans’ Group Life Insurance (VGLI)

- Service-Disabled Veterans Insurance (S-DVI)

- Veterans’ Mortgage Life Insurance (VMLI)

Recognizing that U.S. military members at different ages and stages of career have very different life insurance needs, the VA has developed several programs that can be extremely helpful to service members and veterans.

Let’s take a detailed look at each type of life insurance plan the VA offers so that you can make an informed decision about which life insurance company is best for you and your loved ones.

1. Servicemembers’ Group Life Insurance (SGLI)

The Servicemembers’ Group Life Insurance program offers term life insurance at an affordable cost for eligible members of the U.S. military. Coverage is available up to 400,000 in 50,000 increments. You may be eligible for SGLI if at least one of the following conditions is true:

- You’re an active duty member of the U.S. military, including Army, Navy, Air Force, Marines, and Coast Guard

- You’re a commissioned member of the National Oceanic and Atmospheric Administration (NOAA) or the U.S. Public Health Service (USPHS)

- You’re a midshipman or cadet enrolled in a U.S. military academy

- You’re a cadet, midshipman, or member of a Reserve Officers Training Corps (ROTC) that is currently engaged in authorized training

- You’re a member of the National Guard or Ready Reserve, you’re assigned to a specific unit and your unit is scheduled for at least 12 periods of inactive training per year

- You’re a volunteer in an Individual Ready Reserve mobilization category

- You’re in non-pay status with either the National Guard or Ready Reserve

If you qualify for SGLI, you will automatically be signed up within your service branch, and you can connect with your branch’s HR team for further details. You can then make changes to your account through the SGLI online enrollment system, and your premiums will be deducted from your base pay every month.

2. Family Servicemembers’ Group Life Insurance (FSGLI)

The Family Servicemembers’ Group Life Insurance program extends life insurance coverage to a military member’s spouse and/or dependent children if she’s already covered under full-time SGLI. In addition, one of the following must be true of the military servicemember:

- The servicemember is on active duty

- The servicemember is a member of the National Guard or Ready Reserve

The limits for FSGLI coverage are 100,000 for a spouse and 10,000 per dependent child. Premiums to cover spousal life insurance coverage are taken out of your base pay, while there is no premium for dependent coverage. It is available at no cost to the service member as long as the dependent child is under 18, enrolled as a full-time student, or becomes disabled before reaching age 18. You can sign up for family benefits through the SGLI online enrollment system. You can also make any appropriate changes to your coverage through the online enrollment system.

3. Traumatic Injury Protection (TSGLI)

Servicemembers’ Group Life Insurance Traumatic Injury Protection (TSGLI) is designed to provide short-term assistance for military servicemembers who suffer a severe injury and need financial support. If eligible, you can use this coverage for any injury, no matter whether it occurs while on duty. This protection offers between 25,000 and 100,000 of short-term assistance to those who qualify. To be eligible for TSGLI, you must have been covered by an SGLI policy when injured, and you must meet all of the following requirements:

Servicemembers’ Group Life Insurance Traumatic Injury Protection (TSGLI) is designed to provide short-term assistance for military servicemembers who suffer a severe injury and need financial support. If eligible, you can use this coverage for any injury, no matter whether it occurs while on duty. This protection offers between 25,000 and 100,000 of short-term assistance to those who qualify. To be eligible for TSGLI, you must have been covered by an SGLI policy when injured, and you must meet all of the following requirements:

- You have a scheduled loss that is directly tied to your traumatic injury

- You sustained your injury before midnight on the day you separated from military service

- You suffered a scheduled loss within two years of your service-related traumatic injury

- You have survived for at least seven days following your traumatic injury

- You were an active duty member of the U.S. armed forces, a member of the National Guard, a reservist on one-day muster duty or on funeral-honors duty when injured

If you’re enrolled in SGLI coverage, you also are automatically enrolled in TSGLI coverage and a $1 per month premium will be deducted from your base pay. You should also note that some injuries are not eligible for TSGLI coverage. For example, any self-inflicted wound would be ineligible, along with injuries resulting from use of illegal drugs or controlled substances taken either without the supervision or against the medical counsel of a physician. Injuries are ineligible for TSGLI that result from surgery or that are suffered while attempting to commit a felony, along with injuries that are the result of a physical or mental illness.

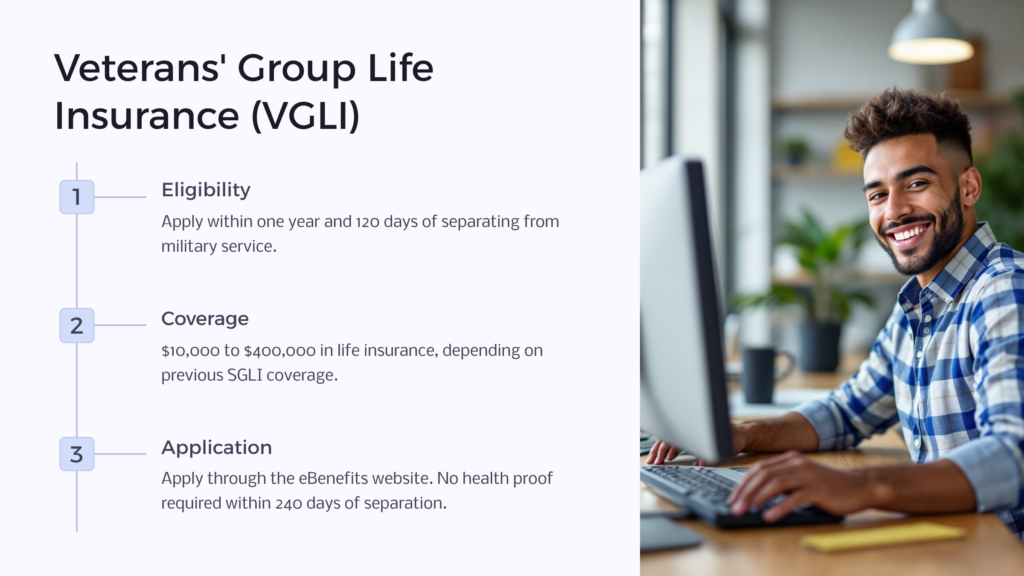

4. Veterans’ Group Life Insurance (VGLI)

When you separate from military service, you’ll need to apply for Veterans’ Group Life Insurance within a year and 120 days after separating. Meeting this deadline will allow you to maintain the same level of coverage you had when on active duty and covered by SGLI, as long as you continue to pay your premiums.

Through the VGLI program, you can qualify for VA benefits of $10,000 to $400,000 in life insurance, depending on what level of coverage you were enrolled in before separating from service. You can increase your coverage by $25,000 every five years until you reach $400,000 in coverage or you reach 60 years of age, whichever comes first. In order to be eligible for VGLI, at least one of the following conditions must be true:

- You were enrolled in SGLI while on active duty and are within one year and 120 days from being released from an active-duty period of at least 31 days

- You were enrolled in part-time SGLI as a member of the National Guard or Reserves and have subsequently suffered an injury that disqualifies you from standard insurance rates

- You are within one year and 120 days of assignment to the Individual Ready Reserves of a particular military branch or to the Inactive National Guard

- You are within one year and 120 days of being placed on the Temporary Disability Retirement List

You should note that if you sign up for VGLI within 240 days of separating from military service, you won’t have to prove that you’re in good health. If you wait any longer, though, you’ll have to submit documentation supporting the claim that you are currently in good health. You will pay a premium for VGLI, depending on the amount of coverage you’d like, along with your age. You can apply for VGLI through the eBenefits website.

At any time, you also can convert your VGLI policy to a civilian policy – you’ll be able to convert at standard premium rates, and you won’t typically have to prove that you’re in good health. You can simply choose a company that participates in our program and apply for civilian coverage through a local agent.

5. Service-Disabled Veterans Insurance (S-DVI)

The Service-Disabled Veterans Insurance program provides low-cost life insurance options for veterans who were rendered disabled because of a service-related illness or injury. In order to be eligible for S-DVI, a veteran must meet all the criteria outlined below:

- You were released from active duty on or after April 25, 1951, without a dishonorable discharge

- You have been rated for a service-related disability, no matter the level of your rating

- You can show documentation that you are in good health, other than your service-related disability

- You apply within two years of the VA giving you a new disability rating

S-DVI typically provides up to $10,000 of coverage. You’ll be charged a monthly premium based on your age, the specific coverage plan you choose, and the level of coverage you’d like. You also may be eligible for S-DVI supplemental coverage if you become 100 percent disabled and unable to work while carrying a basic S-DVI policy. This supplemental coverage offers up to $30,000 in additional insurance coverage.

Some veterans may qualify for a premium waiver. If you are under age 65 and you apply within one year of being notified that you’re eligible for a premium waiver, you may receive this benefit, which amounts to $30,000 of coverage with no premium.

6. Veterans’ Mortgage Life Insurance (VMLI)

If you’ve suffered a service-related injury or other condition that leaves you disabled, you also may qualify for Veterans’ Mortgage Life Insurance. This program allows your loved ones to pay off a mortgage in the event of your death. The plan offers up to $200,000 payable directly to the lender who holds your mortgage.

This includes VA home loans. As your outstanding mortgage amount decreases, so will your coverage, and once your home is paid off, your VMLI coverage will cease. To access VMLI, you also must apply for a VA Specially Adapted Housing (SAH) grant. This grant helps cover expenses related to modifying an existing home to account for a permanent disability – think adding ramps, widening doorways, etc. Once you’re approved for an SAH grant, your loan agent can advise as to whether you also qualify for VMLI and can also help you apply.

Eligibility requirements for VMLI include the following:

- You have a severe, permanent disability that the VA has rated as service-connected

- You have qualified for and received an SAH grant to help modify your home

- You have the title to your home

- You have a mortgage on your home

- You are under age 70

Premiums for VMLI coverage are based on your age, your outstanding mortgage balance, and the amount of coverage you need.

How Do I Sign Up for VA Life Insurance?

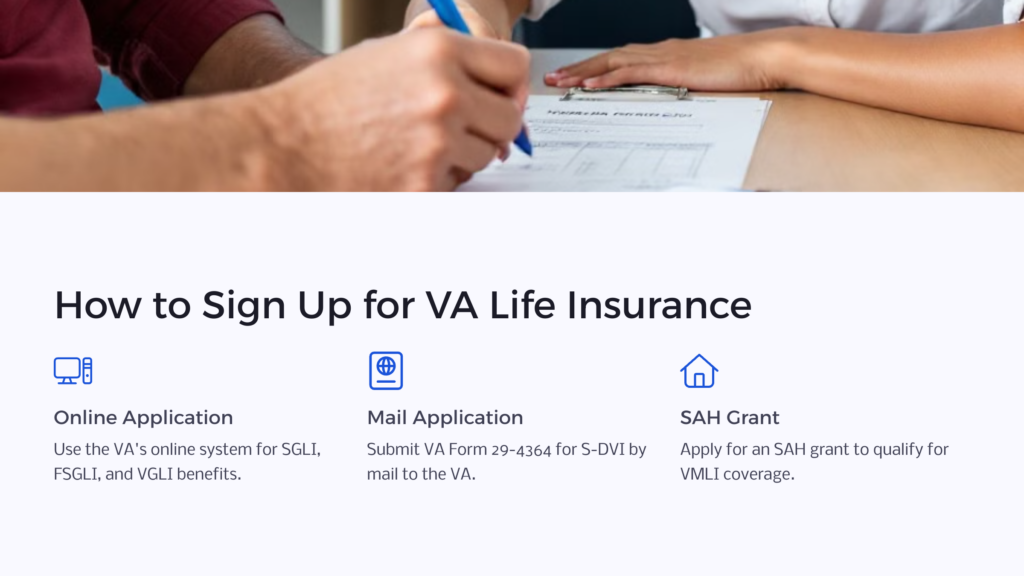

The VA tries to make the process as smooth and easy as possible for both active duty servicemembers and U.S. veterans. In some cases, you don’t have to do anything to sign up for VA life insurance. For example, for SGLI, you’re automatically signed up through your service branch if you qualify, and you can make changes to your account at any time through the VA’s online system. And once you’re enrolled in SGLI, you’re automatically enrolled in TSGLI if you qualify.

For family SGLI benefits, you can sign up through the online benefits system and modify your coverage at any time. The same is true for veterans VGLI benefits. For S-DVI, you can either apply online or submit an Application for Service-Disabled Veterans Life Insurance (VA Form 29-4364) by mail to the VA. For VMLI, you must first apply for an SAH grant and meet VA loan requirements, which you can do through the VA or by mailing your Application in Acquiring Specially Adapted Housing or Special Home Adaptation Grant (VA Form 26-4555) to your regional VA loan center. At this point, your loan adviser will help you sign up for VMLI.

Take Advantage of the VA Life Insurance Benefit

Many of the life insurance programs the VA offers can provide tremendous financial security and peace of mind for each U.S. service member, veteran, and their dependents and loved ones. Make sure to carefully review the information presented here to determine which program is right for you and your family. It’s worth the effort to ensure that your loved ones can be financially secure for the future.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.